For more than a decade, Legal & General (LSE:LGEN) shares have proven a dependable source of passive income. Whatever challenges have come along to knock earnings, the FTSE 100 company has still managed to deliver a large and (largely) growing dividend to shareholders.

Excluding 2020, when the business froze cash rewards as the pandemic rolled on, Legal & General has consistently raised cash rewards for the last 12 years.

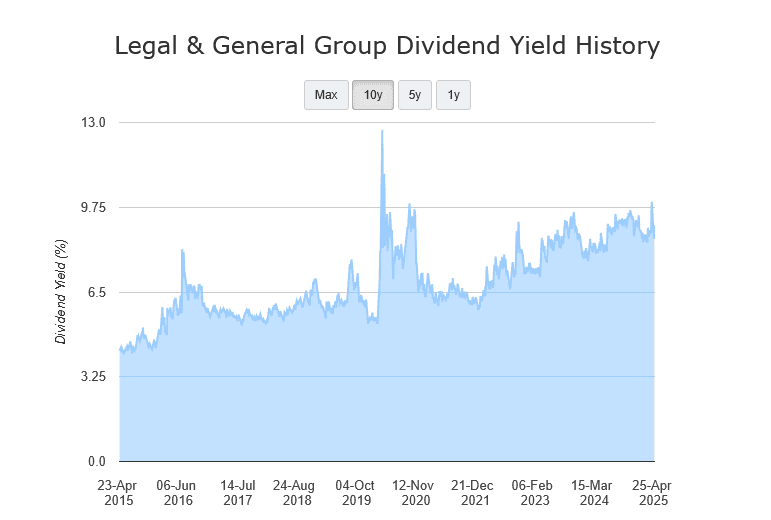

This, in turn, has meant the company’s dividend yields have long towered over the broader FTSE 100 average:

However, past performance isn’t always a reliable guide to future returns. And with threats to the global economy looming, can Legal & General remain one of the London stock market’s greatest dividend shares?

Huge dividend yields

Dividends are never guaranteed. And as we saw during the Covid-19, even Footsie shares with distinguished payout records can cut, postpone or cancel dividends.

But aside from another once-in-a-generation catastrophe, I think Legal & General shares are in good shape to keep delivering a growing dividend. My optimism is shared by City brokers, whose forecasts can be seen below:

| Year | Dividend per share | Dividend growth | Dividend yield |

|---|---|---|---|

| 2025 | 21.82p | 2% | 9.1% |

| 2026 | 22.29p | 2% | 9.3% |

| 2027 | 22.65p | 2% | 9.5% |

These predictions are in line with the firm’s pledge to raise annual dividends by 2% over the period. And it means the firm’s dividend yields sail further above the FTSE 100 long-term average of 3-4%.

Yet it’s important to note that dividend estimates look more than a little fragile based on one popular safety metric. Over the next few years, anticipated payouts are covered between 1.1 times and 1.2 times by expected earnings.

As an investor, I’m seeking a reading of 2 times and above to provide a margin of safety. This can be especially critical for businesses that operate in cyclical industries like this, and particularly today given the tough economic outlook.

Earnings and dividends could disappoint if consumer spending weakens and demand for discretionary products (like life insurance policies) suffers. A deteriorating economy could also dampen returns at Legal & General’s asset management division.

Why I love Legal & General shares

However, its position as a highly-cash-generative business helps to reduce (if not eliminate) this problem. At the end of 2024 its Solvency II capital ratio was 232%, up 8% year on year, and miles ahead of the 100% level required by regulators.

These robust financial foundations are also allowing Legal & General to engage in substantial share buybacks alongside paying market-leading dividends. The business repurchased £200m worth of shares last year, and plans to bump this up to £500m in 2025.

The question for long-term investors like me is can it keep this record up beyond the medium term? I think it can, which is why I own Legal & General shares in my portfolio.

Helped by its tremendous brand power, I think profits and cash flows will boom as demographic changes drive demand for its asset management and retirement products. This in turn could deliver significant dividend income as well as capital gains. I think the FTSE firm’s worth serious consideration today.