Over the long term, oil producers like Shell (LSE:SHEL) have proven to be reliable and generous dividend shares for investors.

Oil companies tend to generate enormous cash flows, and especially when crude prices spike. This often gives them oodles of capital to return to shareholders through dividends and share buybacks.

But can Shell continue delivering large dividends as threats grow? Let’s take a look.

Dividend revival

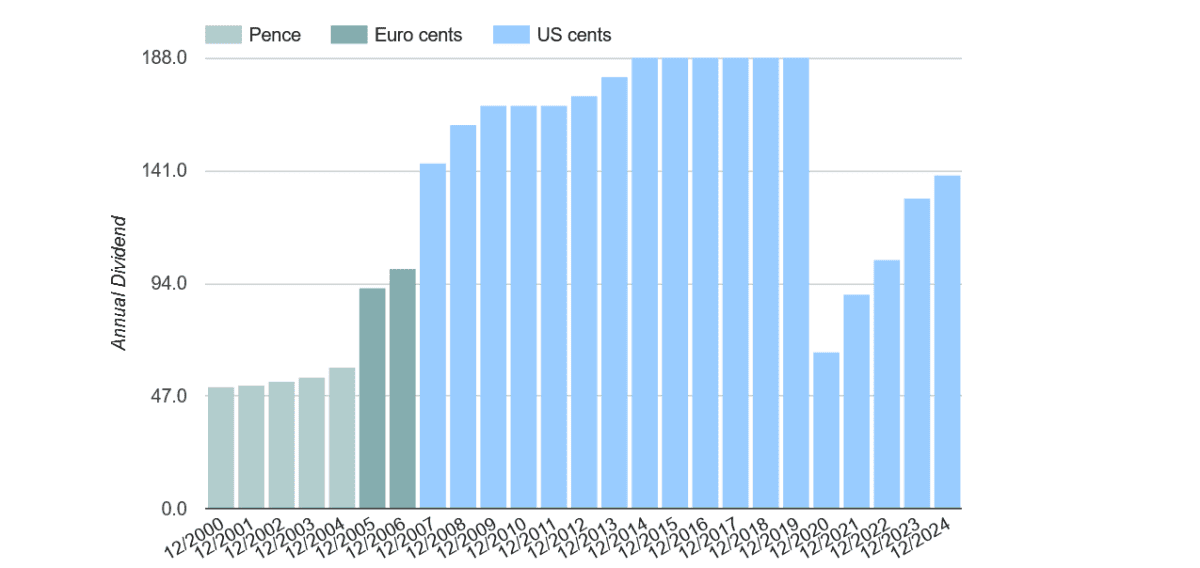

As you can see, annual dividends at the Footsie firm have risen sharply after they were sliced back in 2020. That was the first payout cut since the Second World War.

City analysts are expecting cash rewards from Shell to continue their recent revival, too, as shown below:

| Year | Predicted dividend per share | Dividend growth | Dividend yield |

|---|---|---|---|

| 2025 | 1.43 US cents | 2.9% | 4.4% |

| 2026 | 1.508 US cents | 5.5% | 4.7% |

| 2027 | 1.581 US cents | 4.8% | 4.9% |

According to forecasts, dividend growth is tipped to slow following 2024’s hefty 7.5% hike. However, payouts are still expected to rise above the 1.5%-2% range forecast for the broader FTSE 100 average over that time.

In addition, dividend yields range well above the index’s long-term average of 3%-4% through the next few years.

Balance sheet worries

I’m not prepared to take these projections at face value, though. Firstly, I want to see how well they’re covered by expected earnings given the rising gloom around oil prices.

Encouragingly, Shell scores well on this front, with dividend cover ranging from 2.5 times to 2.6 times. A reading of 2 and above provides a wide margin of security for investors.

That said, I am more than a little concerned about the condition of Shell’s balance sheet and what this could mean for dividends.

Falling oil prices meant cash flow from operating activities slumped 44% year on year to $9.3bn in the first quarter. Meanwhile, net debt jumped by $1bn, to $41.5bn.

Should I buy Shell shares?

Looking ahead, Shell remains confident about the level of cash it will return in dividends over the medium term.

In March, it announced plans to raise shareholder distributions “from 30-40% to 40-50% of cash flow from operations” through a combination of dividends and share buybacks. Accordingly, it’s just announced plans to repurchase $3.5bn more shares over the next few months, and to pay a 0.358-US-cent dividend for the first quarter.

However, there’s a real danger in my opinion that dividends over the next few years could still disappoint. On the plus side, Shell’s strategic and operational record is far better than that of rival firms including BP. And it plans to accelerate cost-cutting measures to protect itself from oil market volatility.

Yet given the uncertain crude price outlook and rising debts, dividends may come under pressure regardless. The cash-sapping nature of Shell’s operations add further danger to forecasts, too (capital expenditure in 2025 alone is tipped at $20bn-$22bn).

As a long-term investor, I’m also concerned about dividends beyond 2027 as renewables erode oil’s share of the energy market. This naturally could also have huge implications for Shell’s share price.

On balance, I’d rather find other passive income shares to buy despite Shell’s market-beating yields.