Building passive income in a Stocks and Shares ISA can look deceptively simple. Buy quality shares, reinvest the dividends, and allow compounding to build momentum over time.

But there’s one factor many investors still underestimate: how costly delaying can become. Even the best long-term investing strategy becomes less effective if investors spend years waiting for the ‘perfect’ moment to begin.

That’s because successful passive income investing relies not just on owning strong businesses, but also on giving those investments enough time to compound.

The hidden cost of waiting

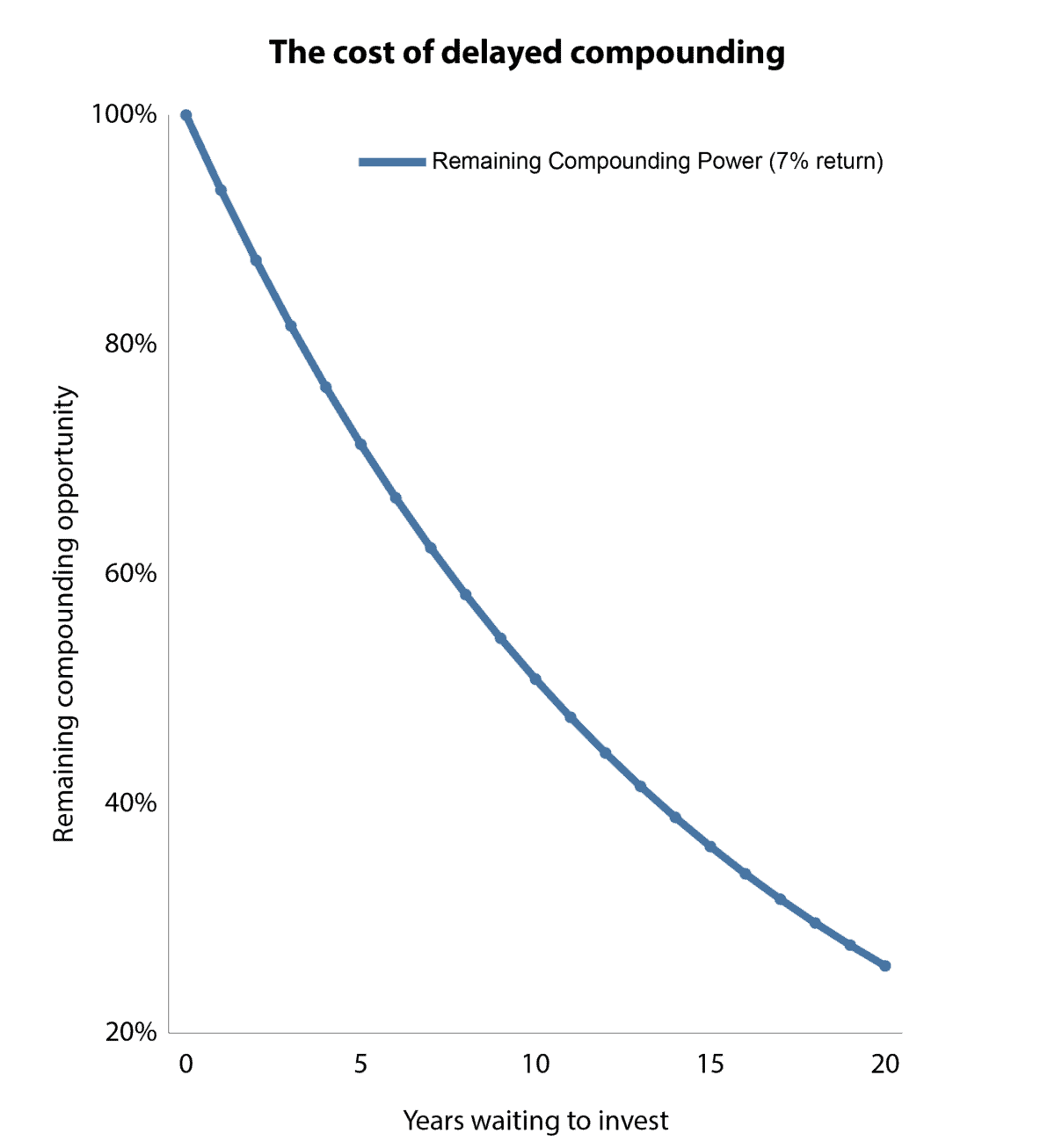

Compounding is usually shown as an upward-sloping chart. Invest early, stay invested, and wealth can grow significantly over time.

But the chart below flips that idea around. Instead of showing how wealth grows, it shows how much of the full compounding opportunity is still available depending on when an investor starts.

The decline is steeper than many investors realise. Assuming a 7% annual return over 20 years, an investor starting today has 100% of the available compounding opportunity. Wait five years and that falls to roughly 71%. By year 20, only about 26% of the original compounding opportunity remains for someone just starting at that point.

That’s because compounding is exponential. The earliest years carry disproportionate weight, as returns themselves begin generating further returns over time. Once those early years are gone, they cannot be recovered.

Which is why building passive income is not just about selecting strong dividend shares. It’s also about giving those investments enough time to compound.

Chart created by author

Stock compounder

The good news is that compounding isn’t limited to high-growth or speculative stocks. High-quality dividend shares that steadily grow earnings and cash flows can also become powerful long-term wealth builders when given enough time.

One FTSE 100 stock I believe fits that description well is Aviva (LSE: AV.)

The insurer is often viewed primarily through its headline dividend yield of 6.3%. But that framing misses how the business actually creates long-term value.

A clear strategic shift towards capital-light businesses, including wealth management and insurance, is improving returns on capital. Put simply, less capital is now required to generate each pound of earnings.

In addition, the group has resumed share buybacks and set new three-year targets running to 2028, centred on more than £7bn of cumulative cash remittances and stronger returns on equity. These cash flows underpin the company’s ability to support and grow shareholder returns over time.

In effect, value is created at two levels: through direct distributions to shareholders, and through reinvestment into higher-return areas of the business. That’s what makes this more than just a yield story.

What could go wrong

As a large insurer, Aviva remains exposed to financial market conditions, including interest rates and equity markets. These can influence both investment returns and capital generation.

Longer-term assumptions around longevity and insurance liabilities also remain a structural feature of the business model. Mispricing these risks can significantly dent profits.

However, taken together, the shift towards higher-quality earnings and strong capital return potential means the shares still look like one to consider for long-term compounding portfolios.

And crucially, as the earlier chart showed, delaying investment can quietly reduce the compounding opportunity available over time — making the timing of getting started just as important as the stock itself.