Quite a few growth stocks are trading at unusually cheap multiples right now. And that might present some big opportunities.

In some cases, falling share prices reflect deep long-term uncertainty. But in other cases, the challenges look temporary.

What’s the stock?

The stock is Danaher (NYSE:DHR). The company is a provider of equipment, software, and services used in drug discovery and development.

The firm has a nice business model. Ongoing consumable sales generate reocurring revenue, while an installed equipment base makes switching difficult.

Drug discovery is also a regulated industry where reliability matters more than price. So quality businesses – like Danaher — can achieve strong margins.

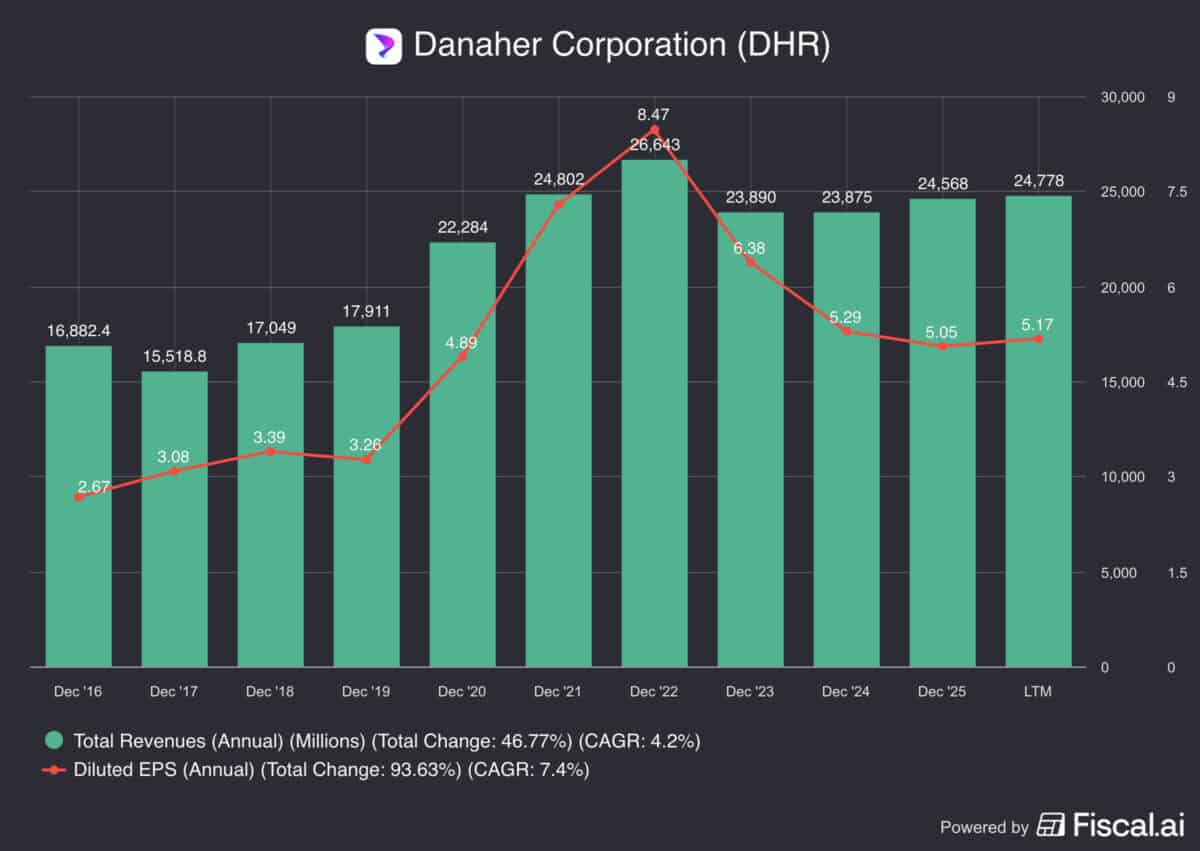

Source: Fiscal.ai

Despite this, both revenues and earnings per share have gone nowhere since 2021. So what’s been going wrong?

Five-year issues

One reason for Danaher’s difficulties is demand for bioprocessing equipment has fallen. It surged during Covid-19, but it’s been weak since then.

Customers have been looking to use their existing supplies, rather than buying new ones. And that’s been weighing on Danaher.

The other issue is that the firm made some dubious acquisitions. These include paying a high price for an mRNA business at a cyclical peak.

That looks like a mistake. But while it’s been weighing on earnings recently, I think there are clear reasons for positivity ahead.

A positive outlook

In terms of demand, Danaher’s bioprocessing unit is starting to show some encouraging signs. The latest update reported a 30% increase in orders.

That’s following two consecutive years of declines, so the basis for comparison is pretty low. But it’s definitely a move in the right direction.

In terms of acquisitions, the firm has a very good record. And that’s not an accident – it’s the result of the Danaher Business System.

This is a set of operating principles focused on efficiency and continuous improvement. Management uses these to help subsidiaries develop.

It’s not infallible, but its success provides a reason for optimism going forward. And the stock is trading at a five-year low.

Valuation

Stocks like Danaher can be tricky to value. Cyclical downturns mean volatile earnings, which makes the price-to-earnings (P/E) ratio unhelpful.

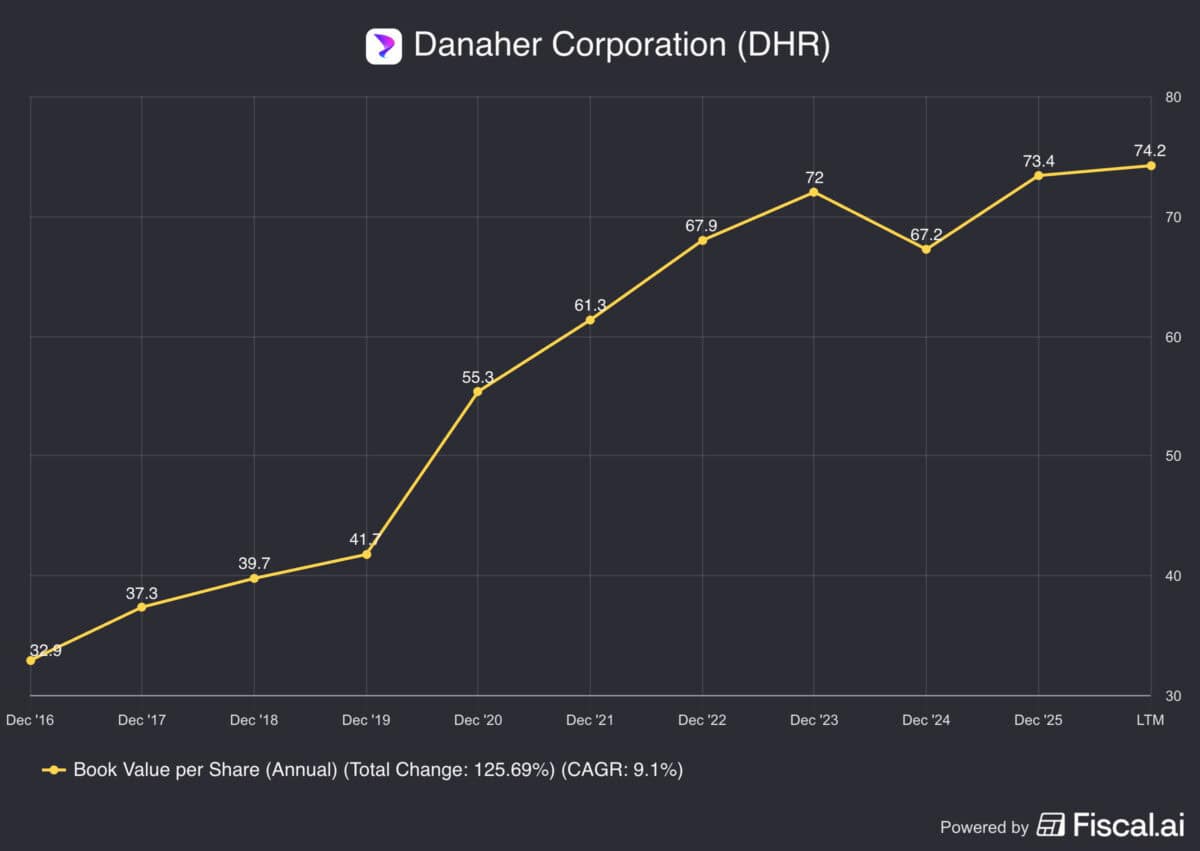

Since the firm retains most of its cash, changes in book value are often a good guide to changes in intrinsic value. And this can be useful.

Source: Fiscal.ai

In the last 10 years, Danaher’s book value has grown by an average of 9.1% a year. That includes the ups and downs of the Covid-19 pandemic.

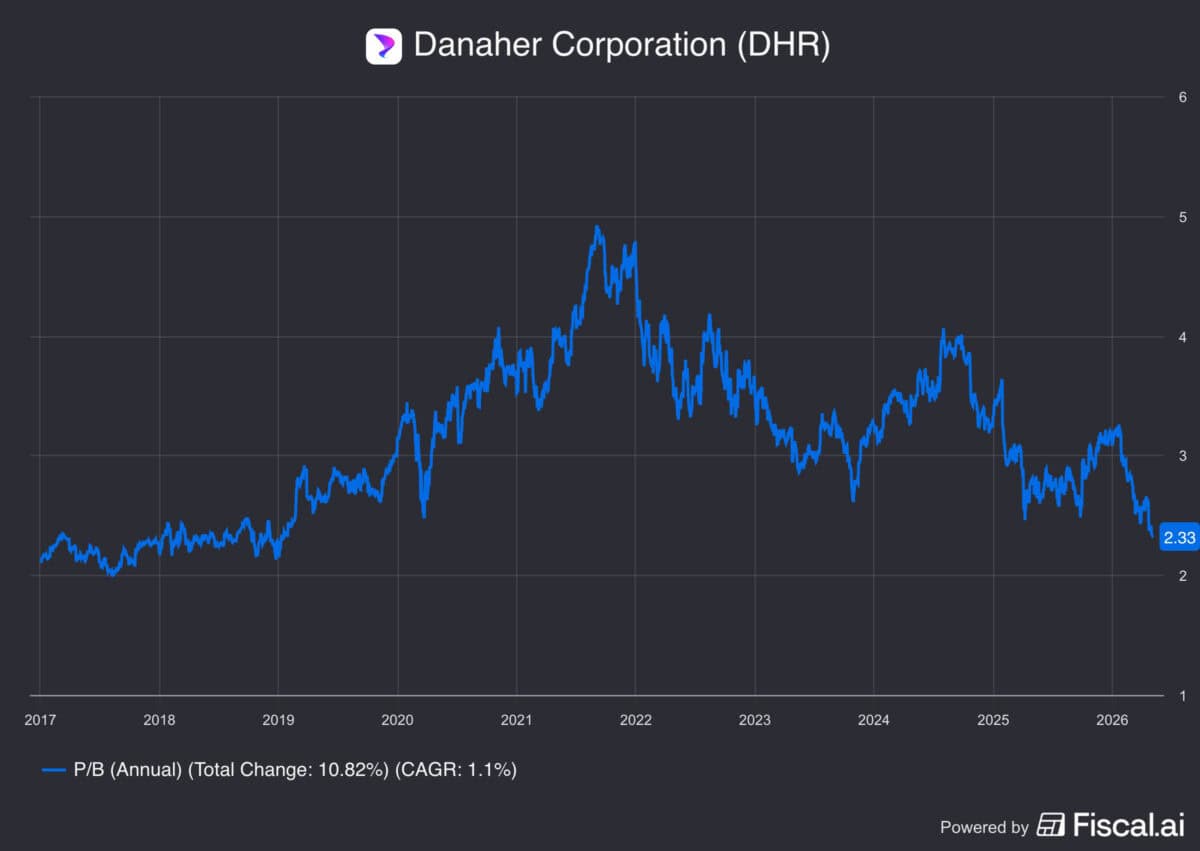

That’s not bad at all. But on top of this, the stock is currently trading at an unusually low price-to-book (P/B) ratio.

Source: Fiscal.ai

Given this, I think there’s real scope for the multiple to expand if growth picks up. And that’s what I’m expecting to happen.

An opportunity

Danaher shares over the last five years have been a lesson in the risks of buying at the top of a cycle. But the reverse is true at the bottom.

That’s why I think growth investors should take a look. This is a business with an outstanding record that looks to be getting back on track.

Does that mean it can’t go lower from here? Absolutely not — but from a long-term perspective, I think there’s a lot to like about the stock at today’s prices.