My investment portfolio is quite heavily slanted towards UK stocks. Many of them are also what we call value stocks.

There are a couple of names that look incredibly cheap initially, but I’m staying well away from them. Why? A closer look reveals some hidden liabilities.

Vodafone: not as cheap as it looks

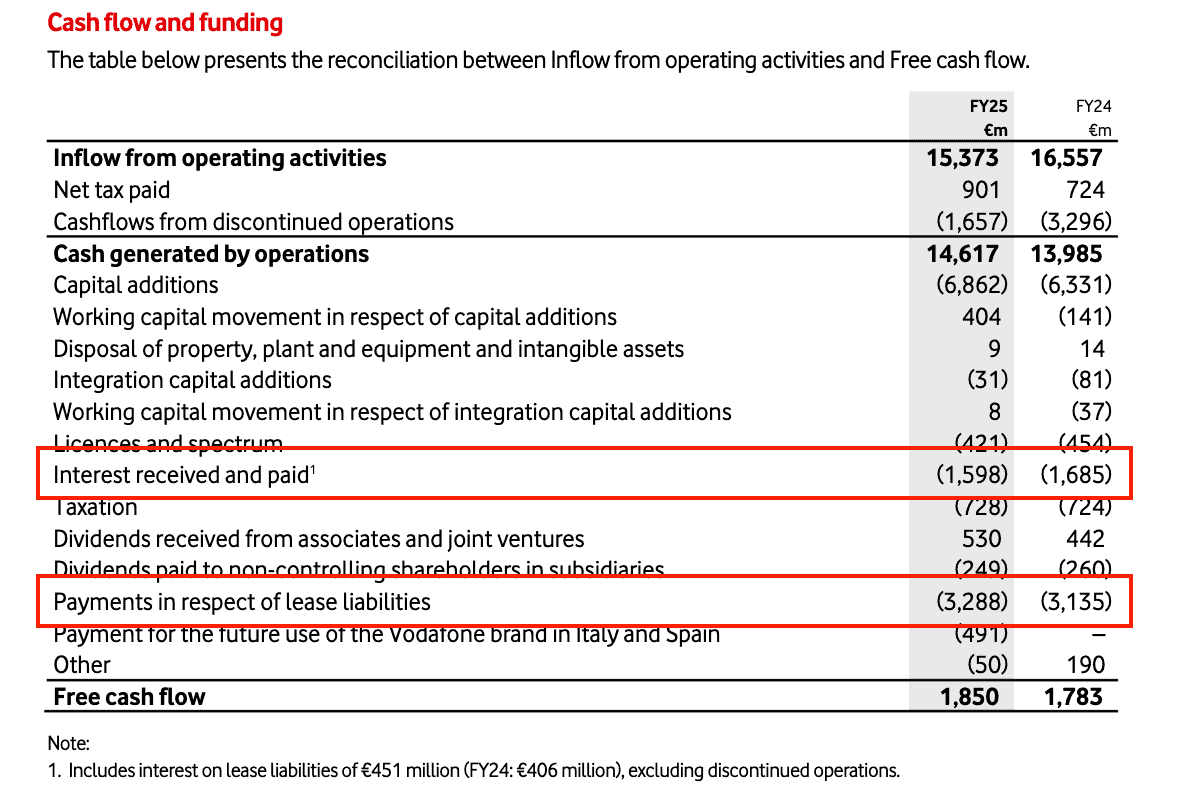

At first sight, Vodafone (LSE:VOD) shares look cheap. On a screener, it shows up as trading at a free cash flow multiple somewhere around 4.

In reality, it’s not that cheap. And this is why investors need to do more than just look at screeners.

Officially, free cash flow is cash from operations minus capital expenditures. In Vodafone’s case, that’s €14bn less €6.9bn.

Set against a €27.2bn market cap, that is indeed a multiple of 3.8. But this isn’t the entire story with this company.

Vodafone’s cash outflows are much more than just its capital expenditures. They include things like interest expenses and lease liabilities.

Source: Vodafone 2025 Annual Report

None of this is a secret. The company presents all of this in its investor materials, but those investors do need to go and find this to figure it out.

Adding all of this in, the firm’s free cash flow is actually closer to €1.8bn. And that implies a multiple closer to 15.

I’m not saying there’s anything wrong with the business. But investors attracted by a low multiple should take a closer look.

easyJet: hidden liabilities

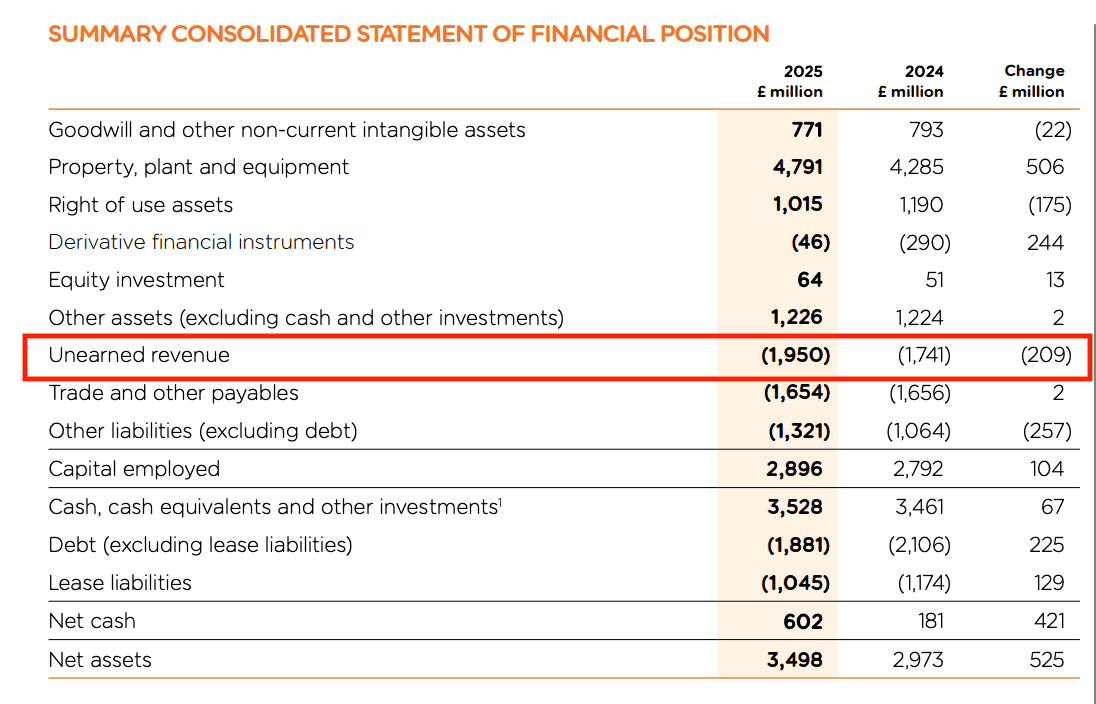

easyJet (LSE:EZJ) is another stock that isn’t as cheap as it looks. On the face of it, the stock looks like a financial fortress.

Again, at first sight, the firm shows up as having more cash than debt. And this is accurate, but it’s not the whole story.

The company has around £2bn in what it calls “unearned revenue”. That’s cash it’s received from customers for services it hasn’t provided yet.

Source: easyJet 2025 Annual Report

This is pretty normal in this industry. Customers usually book their flights and holidays months in advance of going on them.

It’s also a good thing. It means easyJet doesn’t have to use debt to finance its operations – it can use unearned revenues and not pay interest.

These liabilities don’t show up as debt, because easyJet isn’t going to pay customers back. But it is going to have to meet those costs.

Again, there’s nothing wrong with how easyJet reports this. Investors just need to know what they’re looking for.

In the context of a £2.8bn company, £2bn in additional liabilities is a lot. And when I factor this in, I become less interested in the stock.

Hidden risks

UK stocks have a reputation for being cheap. And a lot of them look that way at first sight on a basic screener.

On closer inspection, though, some are less attractive than they seem. So taking a proper look is non-negotiable for investors.

I don’t really use screeners in my own investing. But I’m not against it in principle.

I do think that there’s no substitute for a proper look at a company’s reports. That’s where investors can find hidden risks.

Both Vodafone and easyJet have strengths. But after looking more closely, neither makes it onto my list of stocks to buy.