A £10,000 second income isn’t a fantasy — it’s a maths problem. And like most maths problems, it has a clean solution. You’ve just got to know where to start.

The first number to nail down: how much capital do we actually need?

If we’re targeting £10,000 a year from dividends, the answer depends on the yield we’re earning. At a 5% yield, we’d need a portfolio worth £200,000. At a 7% yield, that drops to around £143,000.

Neither figure sounds trivial.

Of course, we don’t need to save £200,000 from scratch. We need to grow our portfolio — using a Stocks and Shares ISA and a largely underappreciated force: compounding.

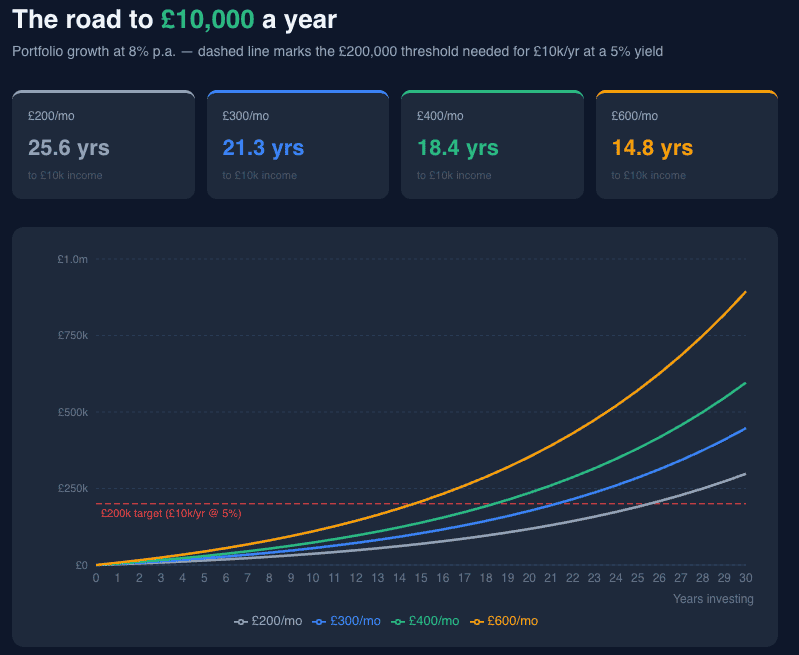

Let’s run the numbers. An investor putting £400 a month into a Stocks and Shares ISA, earning an average 8% annual return, would have a pot worth approximately £235,000 after 20 years. That’s enough, at a 4.5% yield, to spin off £10,575 a year — a genuine second income, sheltered from tax.

The chart below shows how different monthly contributions stack up against the £200,000 threshold:

One aspect that jumps out immediately is the curve.

The first decade of investing can feel thankless. Contributions dominate and growth is modest. But somewhere around years 12 to 15, the compounding effect kicks in hard and the line bends sharply upward. That inflection point is everything.

It also explains why starting early beats saving hard.

An investor contributing £300 per month from age 30 will typically outrun someone putting in £600 per month from age 40 — even though the late starter is doubling down. A decade of compounding is simply very difficult to replicate.

Where to invest?

But here’s something that trips up a lot of investors: building a second income portfolio doesn’t mean holding dividend-paying shares the whole time. During the accumulation phase — the years of growing the pot — many investors actually do better focusing on total return, holding high-growth shares that pay little or no dividend at all.

One stock that I find interesting from a growth perspective, while offering an outsized dividend, is TBC Bank (LSE:TBCG). The Georgian bank has compounded earnings per share at 34% annually since 2020 — yet trades on a forward PE of just 5.2 and has a price-to-earnings-to-growth (PEG) ratio of 0.4.

The forward dividend yield sits at nearly 7%, and that dividend has grown at over 40% a year over the same period, covered almost three times by earnings.

Return on equity of 23.8% and operating margins above 43% tell us that this bank is much more profitable than its UK focused peers. The market simply applies a steep discount for geography: TBC operates primarily in Georgia, and also in Uzbekistan, and that’s where the risk lives.

Specifically, Georgia remains an emerging market with real political volatility. Its proximity to Russia, the instability of the currency against sterling, and the potential for sudden capital flow disruption all mean that the headline numbers can deteriorate fast.

That said, I believe this is an investment worth considering. Georgia’s economy has been the fastest growing in Europe since the pandemic, and TBC still offers good value.