It’s been just over five years since global markets began recovering from the losses caused by Covid. So how much would £5k invested in a Stocks and Shares ISA back then be worth now?

Of course, there’s no precise answer, as it would depend on which stocks were picked. That’s one of the major benefits of a self-directed ISA — they’re fully customisable. We can however, use the FTSE 100’s overall performance as a benchmark.

But first, let’s look at some of the other benefits of this popular British investment account.

The benefits of investing via an ISA

As most already know, a Stocks and Shares ISA allows UK investors to buy shares without handing a slice of the gains to the taxman. This can help supercharge returns over time in a way that standard trading accounts usually cannot.

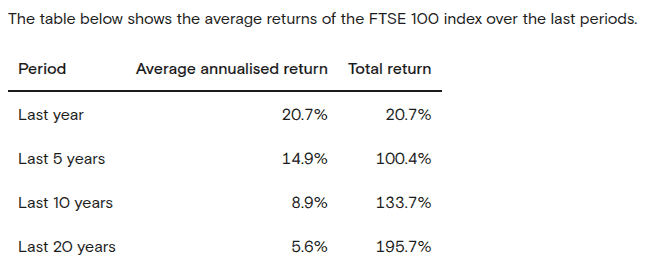

If an investor had put £5,000 into a basic FTSE 100 tracker five years ago, that stake would now be worth close to £10,000 (with dividends reinvested). That’s based on the index’s total return of about 100% over that period (51% without dividends).

Without the ISA wrapper, about £2,000 (or more) could have been lost to taxes. This also reveals the power of compounding by reinvesting dividends.

But history shows these five‑year bursts aren’t the norm. Stretch that same index performance over 20 years, and the annualised return drops to around 5.6%. That’s a far more sobering figure – so how should long‑term investors plan?

Looking ahead

After a strong run, it would be normal to see weaker returns or even a correction. That doesn’t mean a crash is inevitable, but it does mean expectations should be grounded.

Over the next five years, returns could easily be lower than the last five, especially if profits slow or inflation or interest‑rate worries return. That’s where defensive areas of the market can help.

Healthcare, consumer staples and utilities often hold up better when the economy is shaky. People still need medicine, electricity and groceries, whatever the market is doing. One good example is Tesco (LSE: TSCO), and I’ll explain why.

Why Tesco stands out

Backed by its huge UK grocery footprint and strong brand loyalty, Tesco consistently generates healthy cash flow. That’s critical for income investors looking for reliable dividends, which it’s been paying uninterrupted for eight years.

The yield’s only 3% but is well-covered by a payout ratio of only 55% and 4.6 times cash coverage. Plus, the dividend has increased roughly 8% year on year since Covid. In volatile markets, reliability and coverage trumps yield.

A defensive business model further supports this. In tough times, shoppers might cut back on luxuries but they don’t stop buying food. So even when it’s all falling apart, Tesco continues to bring in revenue.

Not that it’s entirely risk-free. Grocery margins are thin, so higher costs, price wars or weaker consumer spending could all hurt profits. Recently, inflation and wage pressure have weighed on its finances – which could threaten the dividend if trading conditions soften.

Still, with a return on equity (ROE) around 13% and a valuation in line with the FTSE average, it looks like a safe option to consider. Boring, sure, but that’s exactly where to find comfort during uncertain times.