With the stock market experiencing a bit of a wobble, now could be a good time to scan for shares to buy. As billionaire investor Warren Buffett says, the best time to invest is when others are fearful.

Here, I’m going to highlight a sub-£2 UK stock that could be worth a look. This name – which has outperformed Rolls-Royce over the last year – appears to offer the winning combination of growth, value, and income.

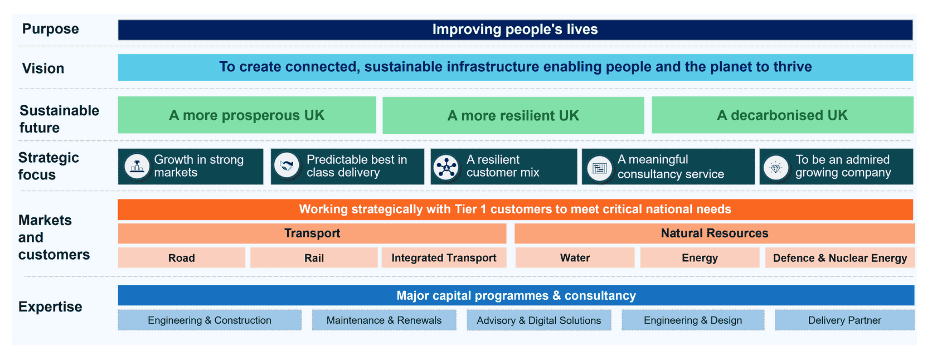

Improving our lives

The business is Costain (LSE: COST), a small British company that specialises in sustainable infrastructure solutions. Operating across the UK’s energy, water, transportation, defence, and nuclear markets, it offers consultancy and advisory services, digital technology solutions, and complex programme delivery. Its ultimate goal is to improve people’s lives.

This stock’s performed really well recently. Over the last year, it’s risen about 80% (versus about 45% for Rolls-Royce). However, like most shares, it’s taken a hit amid the market sell off. Currently, it’s trading for around £1.90, down from £2.03 in early March.

Three top features

Now, as I said at the top, this company appears to offer growth, value, and income. On the growth side, it recently told investors that its forward work position is a record £7bn – almost seven times FY2025 revenue.

Looking at its FY2025 results, it seems the company’s having a lot of success in the energy and defence/nuclear markets right now. Here, revenues were up 39% and 16.5% respectively. Note that for FY2026, analysts expect revenue of £1,233m. That would represent growth of 18% year on year.

“The Group is strongly positioned in structurally growing markets where significant long-term investment is being made to meet critical national needs.”

Costain CEO Alex Vaughan

In terms of the valuation, the forward-looking price-to-earnings (P/E) ratio’s only 12. So the stock looks cheap today, especially when you consider that earnings are rising rapidly (23% growth last year).

Interestingly, analysts at Berenberg just raised their price target to 240p. That’s about 26% above the current share price.

As for income, analysts expect a payout of around 5p per share for 2026. That puts the dividend yield close to 3% at today’s share price.

It’s worth pointing out that investors are also benefitting from share buybacks. Recently, it announced it will buy back £20m worth of stock (about 4% of the float).

One other thing to like is that the share price is in a strong long-term uptrend. Like Rolls-Royce, the stock’s been rising for over three years now.

An opportunity?

Of course, there are risks here. A pullback in government spending in certain areas is one. Last year, the company’s transportation revenues were very weak. This impacted overall performance.

Overall though, I see a lot of appeal in this name. I think it’s worth a closer look right now.

But it’s not the only UK stock that looks attractive at present.