Lloyds (LSE:LLOY) shares have kicked off 2026 in much the same fashion as they finished last year. Up 7% since 1 January, the FTSE 100 bank’s now 70% more expensive than it was a year ago.

Lloyds’ share price has been fuelled by a steady stream of expectations-beating trading updates. Last week it announced underlying profit of £1.9bn in Q4 to keep the run going. This was up 94% and comfortably above City forecasts.

The question is, can the FTSE bank’s shares keep on climbing?

Forecasts

An examination of Lloyds’ profits and dividend forecasts could provide some useful insights on this.

City analysts believe the bank’s earnings will soar 41% in 2026. That’s up from the 13% rise last year. A 20% earnings increase is tipped for 2027.

These hot growth forecasts mean brokers also expect more chunky dividend increases. The 3.65p per share cash reward last year is expected to rise to 4.22p and 4.94p in 2026 and 2027, respectively.

I’m confident Lloyds will pay the dividends analysts are expecting for its shares over the period. Its Common Equity Tier 1 (CET1) ratio was a solid 13.2% at the end of 2025, illustrating the strength of its balance sheet.

On top of this, predicted dividends for 2026 and 2027 are covered between 1.8 times and 2 times by anticipated earnings. These are in and around the security benchmark of 2 and above, and provide added protection in case profits miss forecasts.

But are Lloyds’ growth prospects truly robust? I’m far from convinced.

What could go wrong?

Don’t get me wrong: the bank’s management has been superb at navigating tough market conditions.

As Hargreaves Lansdown analyst Matt Britzman’s noted: “Lloyds is quietly proving itself one of the smartest operators in UK banking… arrears remain low, early warning signs are calm, and impairments are once again impressively contained.“

The problem is that the trading landscape looks set to worsen in 2026. So while the FTSE firm’s been resilient to date, I think it’s gravity-defying act could be on borrowed time. And given how expensive Lloyds shares currently are, I think it’s in danger of a sharp price correction.

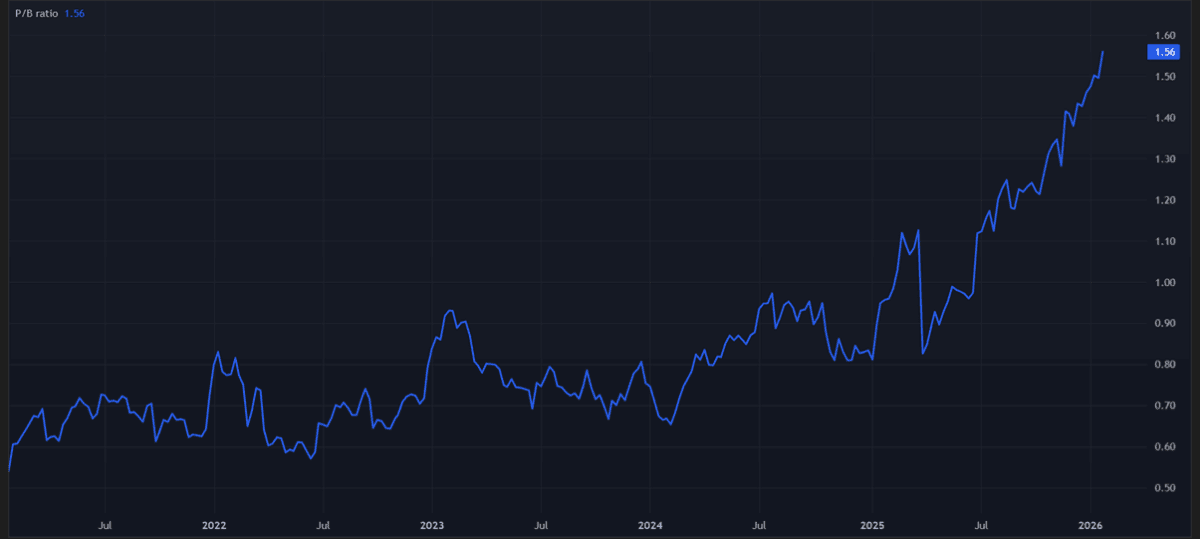

At 106p per share, the price-to-book (P/B) ratio has shot up to 1.6. To put that into context, the 10-year average sits way back at 0.9.

Arguably the biggest risk to Lloyds is the prospect of sharp interest rate cuts, pulling down net interest margins (NIMs). Bank of England action could be especially severe as policymakers act to support the weak economy.

Tough economic conditions are a major threat on their own, naturally. They could drive up impairments and sap income growth. With market competition set to intensify further in 2026, too, income and margins will also come under increased pressure.

Finally, the bank is heavily exposed to the motor finance mis-selling scandal. It’s recently raised provisions to £2bn, but further hikes are possible that could smack the share price.

For these reasons, I’m not planning to buy Lloyds shares for my FTSE 100 portfolio. But having said that, they may be worth a close look from more risk-tolerant investors.