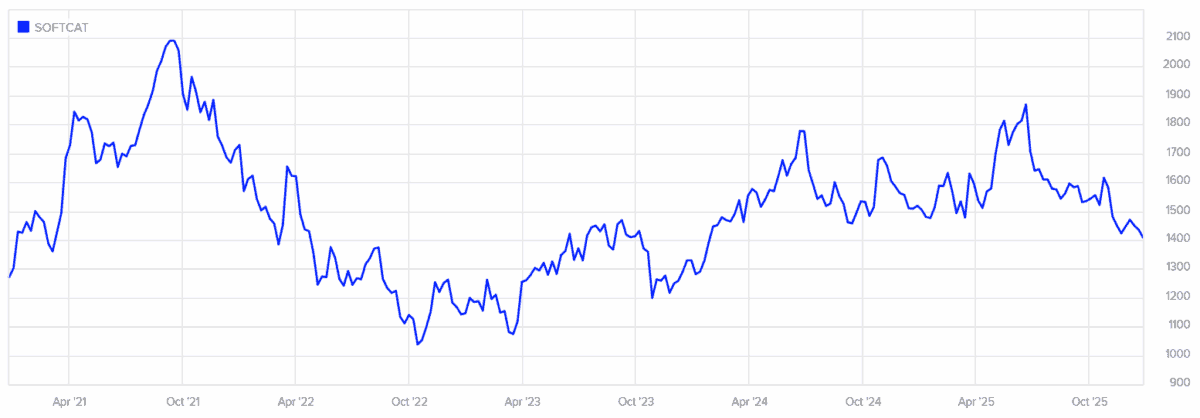

I love a good bargain, which is why I’ve just added growth stock Softcat (LSE:SCT) to my portfolio. Down 20% over six months, Softcat’s price-to-earnings (P/E) ratio has tumbled to 19.8 times. This brings it closer to the industry average, and was a drop I thought too good to pass up on.

But ‘catching a falling knife’ can be risky, and an exciting dip-buying opportunity can turn into a nightmare. With this FTSE 250 stock facing cost and competition challenges, have I set myself up for a fall?

Double-digit growth

First of all, let’s consider why Softcat’s share price has plummeted since the summer. It’s certainly not because trading’s fallen off a cliff. The tech specialist — which has delivered double-digit annual profit growth for 20 years — has continued to pump out forecast-beating numbers.

Gross profit rose 18.3% in the 12 months to July, driven by a 26.8% improvement in gross invoiced income. It followed October’s blowout statement a month later by reporting further double-digit profit growth for the Q1 of this year.

What could go wrong?

Things haven’t been perfect for the FTSE 250 firm though. Costs have risen rapidly (up 19% in the last financial year), and tough market conditions today are slowing bottom-line growth. Looking ahead, competition’s rising that could hamper future contract wins.

Yet Softcat, in my view, has what it takes to overcome these problem and grow profits, as its impressive earnings record shows. Its expertise spans cloud computing, cybersecurity, infrastructure and AI, giving it multiple ways to capture the ongoing digital revolution.

It has a strong balance sheet too to help it capitalise on this opportunity. It put this to good use by acquiring AI specialist Oakland in April, and further M&As are a possibility.

28% price rise?

Of the 12 analysts with ratings on Softcat shares, eight have slapped a Buy or Outperform rating on the company. Two consider it a Hold, and the same number a Sell.

Encouragingly, the average 12-month price target among this group is £18.27 too, representing a 28% increase from today’s levels.

I’m not the only one who’s seen a possible bargain here. Softcat’s chief financial officer Katy Mecklenburgh has also been snapping up shares, purchasing almost £300,000 worth of stock on 8 December. That’s quite the vote of confidence in Softcat’s future prospects. And she bought shares at £14.60 and £14.57 too, higher than the £14.12 I just bought in at.

Bottom line

While Softcat faces challenges, I believe the company’s share price correction since July more than reflects this. My view is that its reduced valuation reflects its lower growth prospects for the near term, and represented an attractive entry point for me to open a position. Its forward P/E ratio’s now at multi-year lows.

Only time will tell if I’ve made a mistake. But for investors seeking potential recovery shares in 2026, I think this growth stock’s worth serious consideration.