Building a £1,000-a-month passive income (£12,000 a year) from an Individual Savings Account (ISA) isn’t straightforward. When I asked ChatGPT for a plan, it flagged the reality: achieving this requires either very high capital or high-return investments, because Cash ISAs alone won’t get you there.

That left me wondering: could a Stocks and Shares ISA bridge the gap and help reach this goal?

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Size of the pot

ChatGPT quickly calculated the pot I’d need to hit my passive income target – and that’s where it went a bit off the rails!

It suggested that with a Cash ISA at 4% growth, I’d need a £300,000 pot. A Stocks and Shares ISA generating 6% yearly returns could reduce that to £200,000.

The confusion came with the difference between total contributions needed and the pot required to safely sustain £1,000 a month. That’s a subtle but crucial distinction for anyone planning income from an ISA.

Crunching the numbers

First, don’t forget inflation. Over time, it quietly erodes purchasing power. Assuming 2% inflation over a 20-year investing horizon, that £1,000 monthly target effectively rises to £1,486.

Using the classic 4% withdrawal rule, the final pot would need to be £445,800.

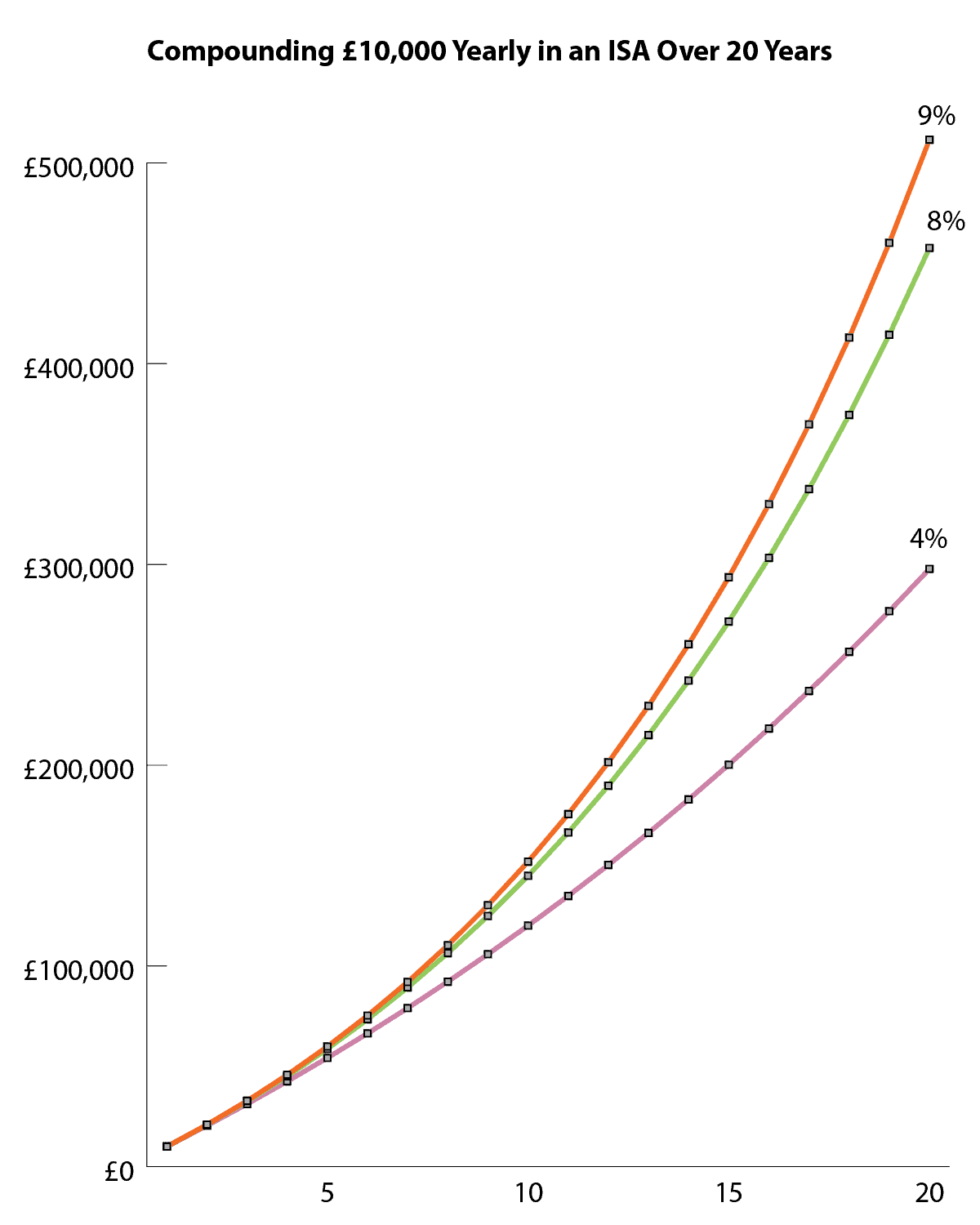

The chart below models £10,000 a year contributions into an ISA over 20 years. It shows that even with a 4% Cash ISA return, the target remains out of reach. But with annual investment returns of 8%-9%, achieving the goal becomes realistic.

Chart generated by author

Constructing a portfolio

Investing isn’t about hitting the target every year – it’s about hitting it on average. Markets deliver good years and bad ones, and that’s unavoidable.

A set-and-forget ETF, like the iShares UK Dividend UCITS ETF, can do a lot of the heavy lifting. It’s had a strong year, combining low double-digit capital growth with a 4.9% dividend yield.

But over the long term, a major bear market can seriously delay recovery – sometimes beyond your investing timeframe. That’s why I don’t rely on one approach. I blend passive investing with active stock picking, targeting high-yield shares for income and a small number of high-conviction growth stocks for long-term outperformance.

A high-yield income stock

Phoenix Group (LSE: PHNX) yields 7.6%, one of the highest dividends in the FTSE 100. Many investors worry about its sustainability because headline IFRS earnings can look weak. For example, last year it generated negative earnings per share.

For insurers, I pay far less attention to those accounting numbers. Profits are distorted by long-term assets backing pensions and life policies.

Instead, I focus on operating capital generation, which strips out the noise. On that measure, the insurer’s cash generation has been strong and, in my view, comfortably supports the dividend.

However, the company relies on stable market conditions and tight cost control to keep funding the dividend. A prolonged market downturn or regulatory change could put pressure on both. Remember, no dividend is ever guaranteed.

Bottom line

For me, building passive income inside an ISA is about patience and balance. I focus on owning high-quality businesses, spreading risk across sectors, and reinvesting income to let compounding do the heavy lifting. Over time, combining reliable dividends with selective growth gives my ISA the best chance to work harder for me.