Amazon (NASDAQ:AMZN) reported Q3 earnings last night (30 October) and the share price soared 13% in extended trading. I’m surprised, but there is a very clear reason why.

AWS – the firm’s cloud computing arm – is seeing an acceleration in revenue growth. And there’s more for investors to be interested in on the artificial intelligence (AI) front.

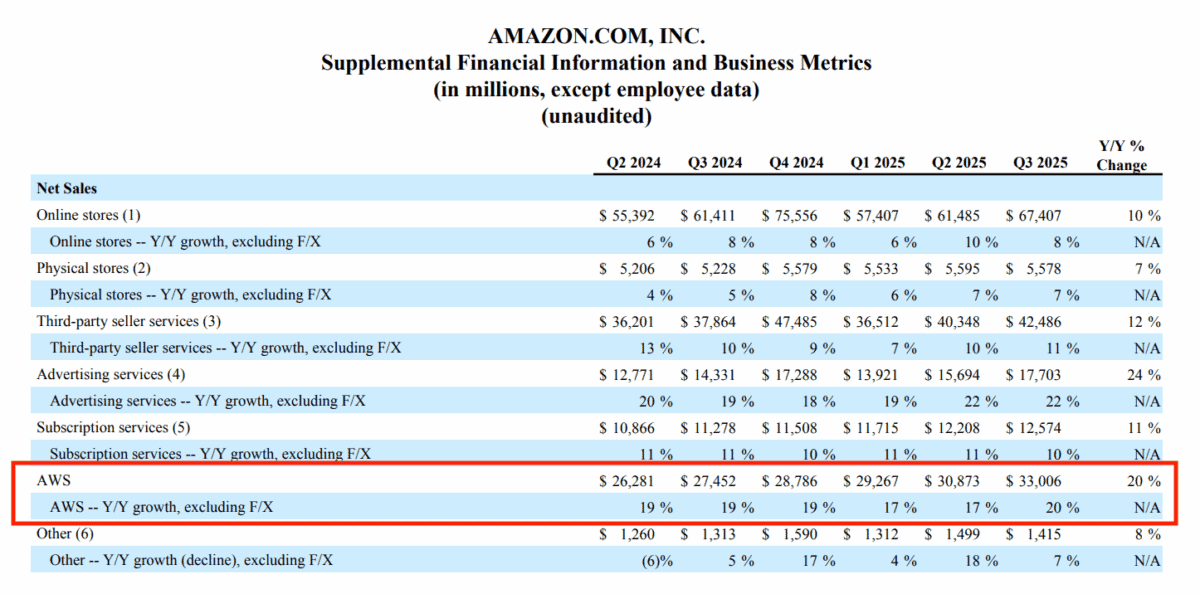

AWS growth

Before the report, I thought AWS revenue growth would be around 17%. And I expected the market to take this badly with Microsoft (40%) and Alphabet (36%) posting higher numbers.

It’s worth noting that AWS is around the size of the other two competitors combined. But its growth has clearly been slower than its rivals and the stock has struggled as a result.

Source: Amazon Q3 2025 Earnings Release

In fact, growth in the cloud business came in at 20% – its best result since 2022. That’s a sign of strong demand and Amazon boosted its capital expenditure forecast to $125bn from $118bn.

There’s a lot to like about AWS and its future growth prospects. But I think one of the most important developments might just be starting to take shape.

Trainium2

Amazon’s report included news of strong adoption of Trainium2, which is the company’s custom AI chip. And this is something I’m focusing on at the moment.

Over the medium term, I expect this to be a major source of growth. Trainium2 has better power efficiency than Nvidia’s Blackwell GPUs, but this comes at the cost of flexibility.

Blackwell’s versatility is valuable in the short term, but I think this will change as applications develop. Once AI roles become more settled, I expect efficiency to become more important.

Importantly, Trainium2 is purpose-built for applications within AWS. So it also creates a significant switching cost for customers who use it in their AI developments.

Risks

Strong results in AWS don’t mean the other challenges facing the business have gone away. And consumer weakness in the US and ongoing tariff concerns are both issues.

Amazon can’t do much directly about either of these issues. But investors looking to assess the importance of the risks should note a couple of things.

The first is that the firm’s scale means it’s better-placed than its rivals to weather a downturn. So weak consumer spending might actually strengthen the company’s long-term position.

The second is that Amazon has been looking to reduce the size of its workforce recently. And this should go some way towards offsetting the rising costs associated with tariffs.

Outlook

Amazon is one of the largest investments in my Stocks and Shares ISA. And I think the latest results are very positive for the company.

Seeing growth accelerating in the cloud computing business is an encouraging sign. And I’m really interested in the adoption of Trainium2 chips as a source of long-term growth.

While AWS is – rightly – the current focus, I’m also impressed at the 24% revenue growth generated by the advertising division. That’s something I think is also worth attention.

I had hoped the share price might fall after earnings, giving me a buying opportunity. But even though that hasn’t happened, I still think the stock is worth considering.