Looking for top growth shares to buy at low cost? Here are two top contenders to consider.

Heading higher

Defence shares like QinetiQ (LSE:QQ.) are surging as European arms budgets sharply increase. This particular FTSE 250 contractor — which has soared despite a profit warning in May — has risen 21% in value so far in 2025.

Yet QinetiQ shares still look dirt cheap, in my view. City analysts expect earnings to rise 18% in the current financial year (to March 2026), resulting in a forward price-to-earnings growth (PEG) ratio of 0.9.

Any sub-one ratio indicates that a stock is undervalued.

Recent problems Stateside meant QinetiQ’s earnings fell 11% in financial 2025. But the business is tipped to deliver sustained growth from this point on. Bottom-line rises of 13% and 10% are also being tipped for 2027 and 2028, respectively.

Uncertainty over US defence budgets going forwards remain a threat. But the company hopes restructuring there — including the recently announced sale of its US Federal IT Services unit — will draw a line under recent problems and reduce exposure to more volatile short-cycle projects.

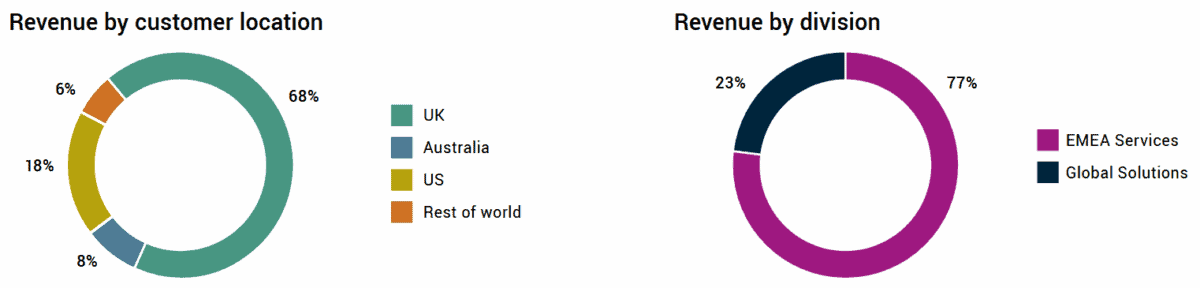

On balance, I believe QinetiQ’s outlook is robust as broader defence spending among NATO and associated partners increase. The company’s order book swelled to £2bn as of March, up 12% year on year, as its diversified global footprint helps offset troubles in the US.

I think QinetiQ’s a top way to consider gaining exposure to the otherwise expensive defence sector. It’s also worth noting the company’s forward price-to-earnings (P/E) ratio is 16.4 times, below those of FTSE 100 industry players BAE Systems (26.6 times), Rolls-Royce (41.5 times), and Babcock International (21.3 times).

Doubled in value

Gold stocks are another asset class I think growth investors need to look at. I myself own an exchange-traded fund (ETF) of multiple metal producers as gold prices soar (they’re up 40% over the last 12 months alone).

Bullion reached new record peaks around $3,700 per ounce just this week. Further gains are tipped as inflationary and growth fears climb, and the US dollar faces sustained pressure.

One cut-price gold stock I believe merits close attention today is Pan African Resources (LSE:PAF).

City analysts think earnings will rise 62% in value this financial year (to June 2026) as gold prices rise and the miner’s production increases.

The company’s exciting growth projects include the Mogale Tailings Retreatment (MTR) and Evander projects in South Africa, and Tennant Mines in Australia. Remember that production issues are a constant threat that could impact earnings.

Today, Pan African shares trade on a forward P/E ratio of 7.1 times. They also carry a rock-bottom PEG multiple of 0.1. I don’t think these figures reflect the gold miner’s supreme growth prospects, and expect the company to continue rising in value. Its shares have risen 125% so far in 2025.