When hunting for dividend stocks, it’s tempting to chase the highest yields. But a generous dividend means little if the company behind it is financially stretched or operating in a declining sector. What really matters is a blend of yield, dividend growth, consistent payments and strong fundamentals.

It’s also worth remembering that dividends are never guaranteed. If business conditions turn sour, even the most established companies can reduce or scrap their payouts altogether. That’s why its critical to do a full assessment before making any investment decisions regarding dividends.

One FTSE 100 stock that currently ticks a lot of the right boxes for me is LondonMetric Property (LSE: LMP).

A quiet performer with a solid yield

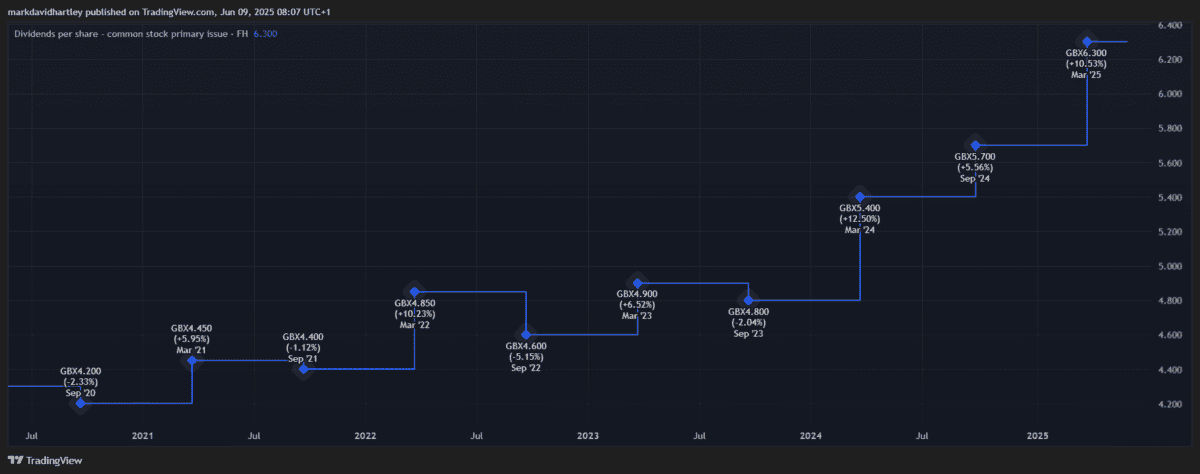

Londonmetric’s a real estate investment trust (REIT) that specialises in logistics, retail parks and long-income assets. Currently sitting around 6%, its dividend yield has maintained a steady position between 5% and 7% for the past year.

Most promisingly, it’s grown its payout every year for the past decade – a rare track record, even among blue-chips. But what exactly is a REIT and why are they good for dividend income?

Regulated returns

REITs are a specific type of company structure that focuses on owning and managing income-generating real estate. Under UK law, they’re required to distribute at least 90% of their property rental profits to shareholders. This is why they’re typically a popular choice among income-focused investors.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

LondonMetric’s focus is on sectors with structural demand tailwinds, such as e-commerce warehouses and out-of-town retail. These assets tend to have long leases and lower vacancy risks, offering some resilience during economic downturns.

This mix of long-term reliability and regulated profit distribution makes it a particularly attractive prospect.

What’s the catch?

No investment is risk-free, and LondonMetric’s no exception. Interest rate changes can impact both property values and debt servicing costs. Additionally, any major financial crisis would be a significant threat, particularly in the real estate sector (anyone remember 2008?).

The trust’s emphasis on logistics and long-lease assets offers some insulation. But no company can future-proof itself entirely from unexpected environmental or geopolitical factors.

Recent performance and financials

Looking at Londonmetric’s latest results, earnings per share (EPS) rose 3% and rent collection remains strong at over 99%. The company also reported a stable portfolio value, with asset management initiatives and rental uplifts helping to offset valuation pressures from rising interest rates.

Its dividend cover sits at 70%, which is modest but typical for REITs. The balance sheet appears healthy, with a loan-to-value ratio of around 32%, comfortably below sector averages.

Slow and steady

Londonmetric’s share price has barely moved in the past year, but it still delivered a return of 8.3% with dividends. If the UK property market enjoys a notable recovery, this figure could rise above 10%.

It’s an example of how reliable dividend stocks play a vital role in building long-term wealth. No-brainer buy? Maybe not. But with a solid yield, a strong track record and exposure to high-demand property segments, I believe LondonMetric’s worth considering as part of an income portfolio.

That said, no single stock should carry the load. Diversification remains key – across sectors, asset types and geographies – to reduce risk and keep those dividend streams flowing, even when markets turn sour.