FTSE 100 conglomerate Halma (LSE:HLMA) issues its full-year results on Thursday (12 June). And I’m going to be watching very closely when it does.

I think the firm is one of the UK’s top growth stocks, but it also trades at a share price that reflects this. So I’m on the lookout for a potential buying opportunity.

Company

Halma is a collection of safety businesses with a distinctive structure. It operates as a decentralised conglomerate, meaning individual subsidiaries make their own decisions.

This helps preserve an entrepreneurial culture, rather than one where everything goes through a central office. The benefits of this are speed, agility, and a closer focus on customers.

In terms of growth, it means Halma has two main sources of opportunity. One involves finding ways to improve its existing businesses and the other involves acquiring new ones.

This is a formula that has generated a huge amount of success for the company over the long term. Over the last decade, revenues have grown at an average of more than 11% per year.

Growth stocks

Halma’s outstanding performance hasn’t gone unnoticed by the stock market. As a result, the stock trades at a price-to-earnings (P/E) multiple of 39, which is more than double the FTSE 100 average.

That’s based on the statutory earnings per share, rather than the adjusted numbers the company provides. But even on an adjusted basis, the P/E ratio is still 33.

A high multiple means there’s a risk of the share price falling if the company’s growth disappoints investors. And there are a couple of key metrics that investors should pay attention to on this front.

Revenue growth is extremely important, but there’s something else investors need to focus on. Halma’s acquisition-based strategy is intrinsically risky and this is worth paying attention to.

The key numbers

Acquiring other companies is almost certain to generate revenue growth. But there’s always a risk of overpaying for a business, which can be destructive to business health and shareholder value.

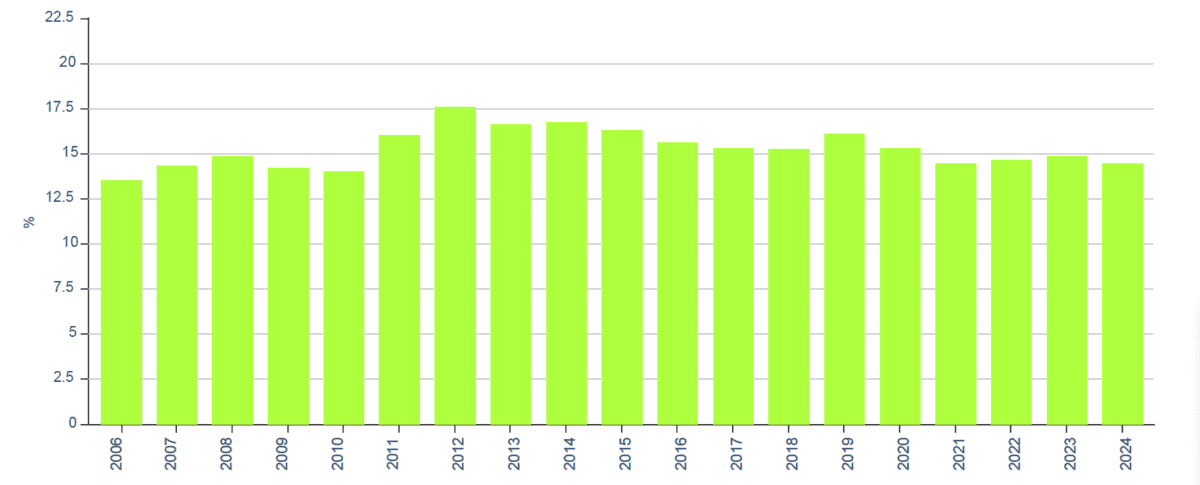

That’s why investors have to pay attention to how effectively the firm is using its capital. And Halma reports this via its Return on Total Invested Capital metric.

Halma Returns on Total Invested Capital

Source: Halma Investor Relations

The company aims to achieve returns above 12% and it has done this very effectively in the past and this is the result of skill, not luck. This has been the foundation of the firm’s success.

From an investment perspective, it’s important this continues. And – as well as revenue growth – that’s the metric I’ll be paying attention to when Halma releases its results this week.

Being ready

I think its structure and track record make it one of the UK’s best growth stocks, but the share price looks like a fair reflection of this at the moment. The key, however, is being prepared.

Historically, opportunities to buy the stock at a bargain price have been few and far between. And that’s why investors need to be ready when they present themselves.

If the company’s upcoming report indicates that revenue growth is slowing, the share price could fall. But as long as the firm is still achieving strong returns on its investments, it could be an opportunity for me.