Dr Martens (LSE:DOCS), the FTSE 250 fashion bootmaker, has endured a torrid time since making its stock market debut in early 2021. After (it’s hard to keep up) five profit warnings, the group’s shares are now worth 87% less.

But since issuing its third quarter trading update in January, there have only been 12 news releases to the market. Eleven of these have been about the number of shares in issue and stock options. The other concerned the appointment of two non-executive directors. Otherwise, it’s been very quiet.

Is this a case of ‘no news is good news’? Or should shareholders remain anxious?

Let’s take a look.

Openness and transparency

The first thing to note is that stock market rules require any information that’s likely to be used by a “reasonable investor” as part of their investment decision – and could have a non-trivial impact on a company’s share price — to be disclosed.

Based on the Financial Conduct Authority’s guidance about what information companies need to share with investors, I think we can assume that the absence of information means nothing’s changed since the company’s most recent update.

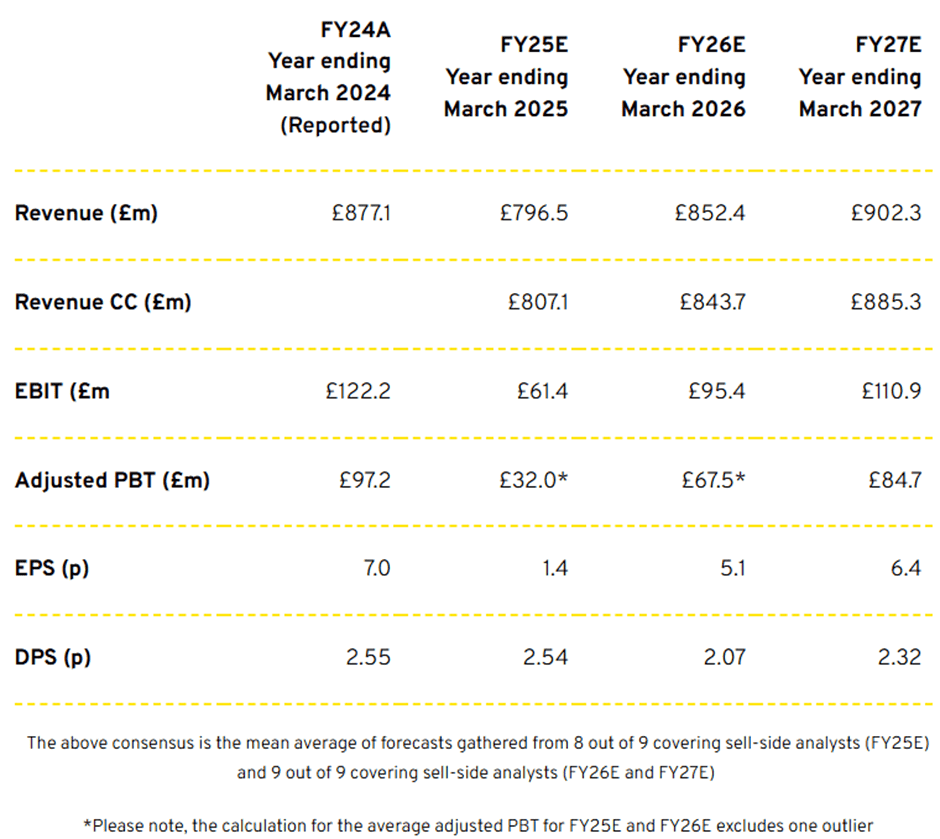

And this reported that trading was in line with expectations. What does this mean?

In April 2024, the company issued guidance on its expected performance for the year ended 31 March (FY25). It warned: “We could see a worst-case scenario of PBT (profit before tax) of around one-third of the FY24 level”.

However, it also said there are “scenarios where the profit outturn could be significantly better than this”.

It’s hard to know what to expect. Based on their latest forecasts, analysts appear to agree with the most pessimistic assessment. The consensus is for adjusted PBT of £32m, which is almost exactly one-third of last year’s figure.

An uncertain outlook

When the company releases its FY25 results on 5 June, I wonder if the share price might react like that of JD Sports Fashion? On 9 April, it released results which were in line with expectations. Since then, its shares have increased 44%. It’s almost as though investors were looking for confirmation that everything’s okay.

And if Dr Martens could beat analysts’ predictions, who knows what might happen to the share price. On the other hand…

That’s why it’s important to take a long-term view. It’s impossible to predict movements from one month to the next.

But looking further ahead, we don’t know what President Trump’s going to do with tariffs. And North America’s a key market for the group. During FY24, 37.1% of revenue came from the Americas. However, the bootmaker doesn’t have any manufacturing facilities in the territory. It’s therefore vulnerable to additional import taxes.

The group also sees the region as a key driver of its future profit. A US economic slowdown could affect earnings.

To try and compensate for post-pandemic price rises, the group’s implemented several price rises in recent years. There are now plenty of cheaper alternatives available which could also affect earnings.

For me, there’s too much uncertainty around to part with my cash. However, I think the company retains a strong brand with a loyal following. Its shares are also cheap by historical standards.

If it does turn things around, there will be plenty to shout about.