The ASOS (LSE:ASC) share price is very low right now compared to historical levels, but does that mean it’s a value share worth buying?

Value investing is tricky because it’s hard to predict accurately if a low share price will rise again.

I aim to find out whether ASOS is down and out or about to get back in the fight.

What is ASOS?

The company is an online fashion and beauty retailer that targets young consumers. Some 45% of its revenue comes from its home UK market.

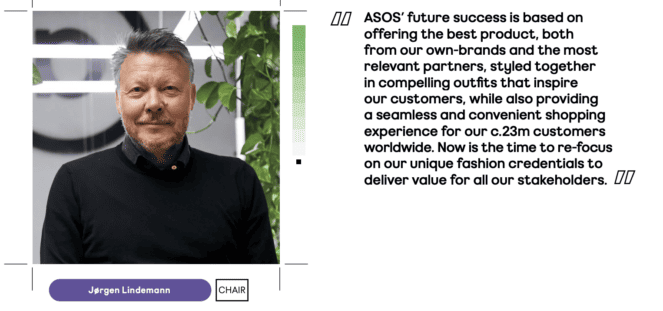

I found this statement from the chair of ASOS, outlining some key figures and the brand’s mission:

Why is the share price so low?

There are a few core reasons why I think the share price has plummeted.

The company has faced revenue growth woes since 2021 after it had boomed during the pandemic. And it reported a recent 11% decline for 2023. That makes me concerned about future growth potential, especially given the increased competition out there from companies like Zalando and Shein.

In response, ASOS launched a £300m cost-cutting plan, including job cuts and the closure of three of its storage facilities.

The sales slowdown hasn’t been helped in the last 18 months by inflation’s effect on customer spending.

Perhaps these issues are short term. Yet there are some deeper concerns I’d like to address before considering investing in the shares.

A big risk

There’s one primary concern that I think makes the company unattractive right now. It keeps issuing new debt. This significantly weakens the organisation’s balance sheet.

In fact, long-term liabilities — or debts due for repayment in more than one year — have gone up from 1% of total assets in 2018 to 67% today.

However, current liabilities — where repayment is due in less than a year — have decreased from 55% in 2018 to 27% today, which is good news.

Could the price rise?

I think it’s going to be difficult for the share price to turn around from here. However, it wouldn’t be the first time the share price has swung from low to high.

It rose 380% from 1,060p in April 2020 to 5,700p in March 2021, primarily driven by a pandemic-linked e-commerce boom. Of course, past price jumps are no guarantee of future results.

But what are some of the strategies ASOS is employing that could spur a rise like this again?

The main direction reinforcing this possibility for me is CEO José Antonio Ramos Calamonte focusing on profit rather than revenue growth. Moving forward, his focus on efficiency could build a more robust financial picture for the company.

That’s even if revenue growth struggles.

And revenue growth has indeed been struggling! In the last year, the growth rate has been negative by over 14%.

Final words

It’s hard to say whether the share price will definitely rise again. Yet I think there’s reason to believe it could. That said, the company is just too risky for my appetite.

I won’t be buying the shares or even adding this one to my watchlist.