The BAE (LSE:BA.) share price is up 140% since 6 November 2020. I’ve analysed what’s been happening so I could decide whether the price is fair and whether it’s a buy for my portfolio.

What is BAE?

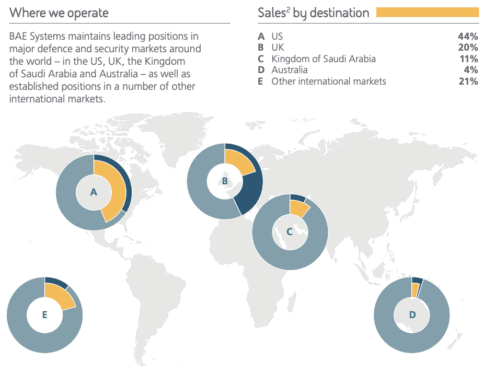

This British organisation operates around the world and specialises in defence, security and aerospace.

It’s a major player that contributes to the production of naval ships, aircraft and advanced electronics.

As the image below shows, it operates in multiple countries with the US its biggest market.

My initial reaction

Of course, it may seem obvious why the shares have risen. When I saw the price of the shares had shot up recently, I thought of the wars that have broken out worldwide.

My instinct told me that investors are piling into BAE Systems shares because they expect revenues to increase and defence spending to go up.

I think their reasoning makes sense. But if active conflicts are the primary cause of BAE share price buoyancy, it would be an issue for me due to ethical considerations.

However, I also believe there are other data-driven reasons for the price increase.

Is the price justified?

My research has confirmed my hunch. For instance, BAE Systems has a record £66bn order backlog amid rising global defence demand.

Part of that backlog is a Czech Republic order for 246 vehicles and a Polish missile contract.

BAE Systems has also been beating earnings expectations, with earnings per share exceeding estimates by a massive 43%.

That said, I don’t feel such an increase justifies the price being up 140%.

I think such a high price assumes we’ll see a massive war and ongoing high expenditure on defence in the next decade.

This isn’t a future I want to see and certainly isn’t one I want to invest in.

Further financial considerations

I have to say, though, that the company’s financial statements do look quite strong right now.

For example, BAE Systems’ total liabilities have decreased from 80% of total assets in 2020 to 65% today. Put simply that means the company has less debt on the balance sheet.

And operating income, which deals with revenue minus all of its operational costs, has risen to 10% of total revenue from 3.75% in 2013.

Still too high for me

To answer my question in the headline, whether the current share price of BAE Systems is too high is relative — it depends personal predictions about the state of the world in the years ahead.

In my opinion, increased demand and strong future estimates, mainly due to the Ukraine and Gaza conflicts, do warrant a higher stock price.

But I’m staying away from the shares. Apart from the ethical implications, the price is already too high (based on the financials) for me.