The Lloyds (LSE:LLOY) share price is at its lowest point in two and a half years. At 40p, shares in the UK’s second largest bank are currently cheaper than they were after the Silicon Valley Bank fiasco that sent financial stocks into meltdown in March.

The vast majority of brokerages have ‘buy’ ratings on Lloyds. In fact, there’s been no ‘sell’ rating published in 2023. That’s a really positive sign.

The average price target is currently 60.7p, representing a 50% increase from the current position. However, Goldman Sach has a price target of 80p — 100% above the current share price.

So, is it realistic to imagine Lloyds hitting 80p? Let’s explore.

Medium-term tailwind

There are several reasons to assume that the next few years will be more lucrative with fewer default concerns.

That’s because interest rates appear to have peaked. And that means we’re likely to see central bank rates fall closer to the so-called Goldilock Zone.

Under normal economic conditions — that is, not a severe recession — lenders theoretically perform best when interest rates are between 2% and 3%.

That’s because they can still achieve strong margins when lending cash, but concerns about customers defaulting fall as interest repayments moderate.

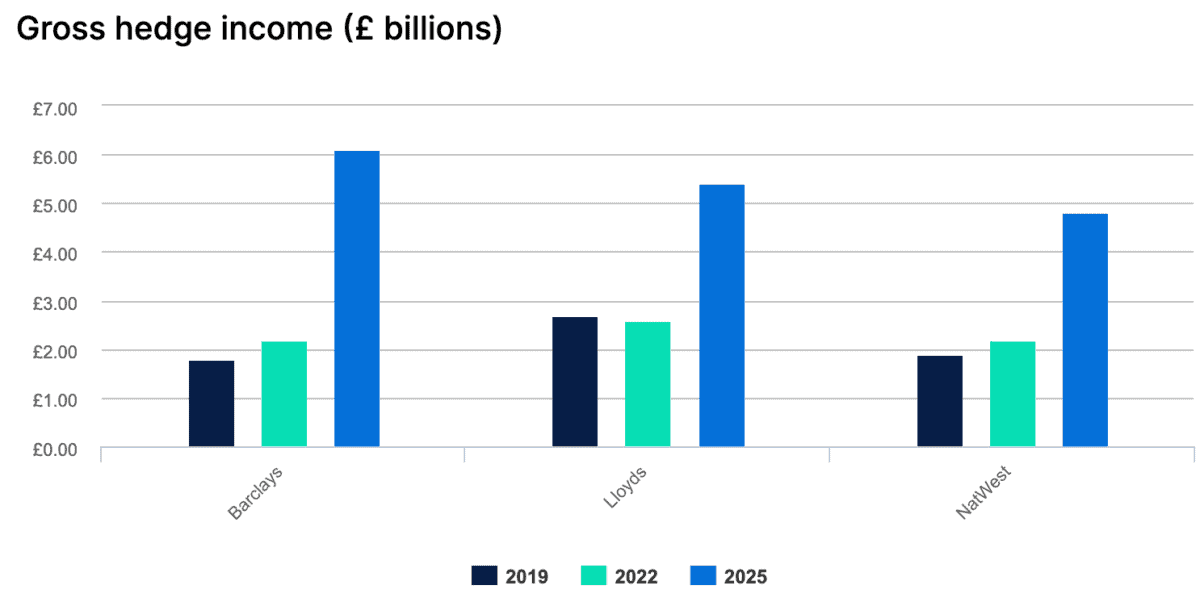

In turn, banks can also benefit from something called a structural hedge. This is where banks allocate their resources to typically fixed income assets, in order to reduce the impact of interest rate fluctuations.

Additionally, this strategy provides an advantage when interest rates peak and start falling.

For instance, in the context of a bond portfolio, lower-yield bonds that mature can be replaced with higher-yield bonds, effectively creating a cushion against the impact of falling interest rates.

And we’re not talking small figures. The hedge boost is highlighted in the Hargreaves Lansdown research below.

Valuation

Lloyds shares are being pulled down for several reasons. This includes negative outlooks on the UK economy, unrealised bond losses, and the threat of widespread credit defaults.

Personally, I’m not concerned about unrealised bond losses. However, a recession in the UK could really do damage to the lending market.

Nonetheless, these risks, which I believe are rather overblown, contribute to the very attractive valuation of the company.

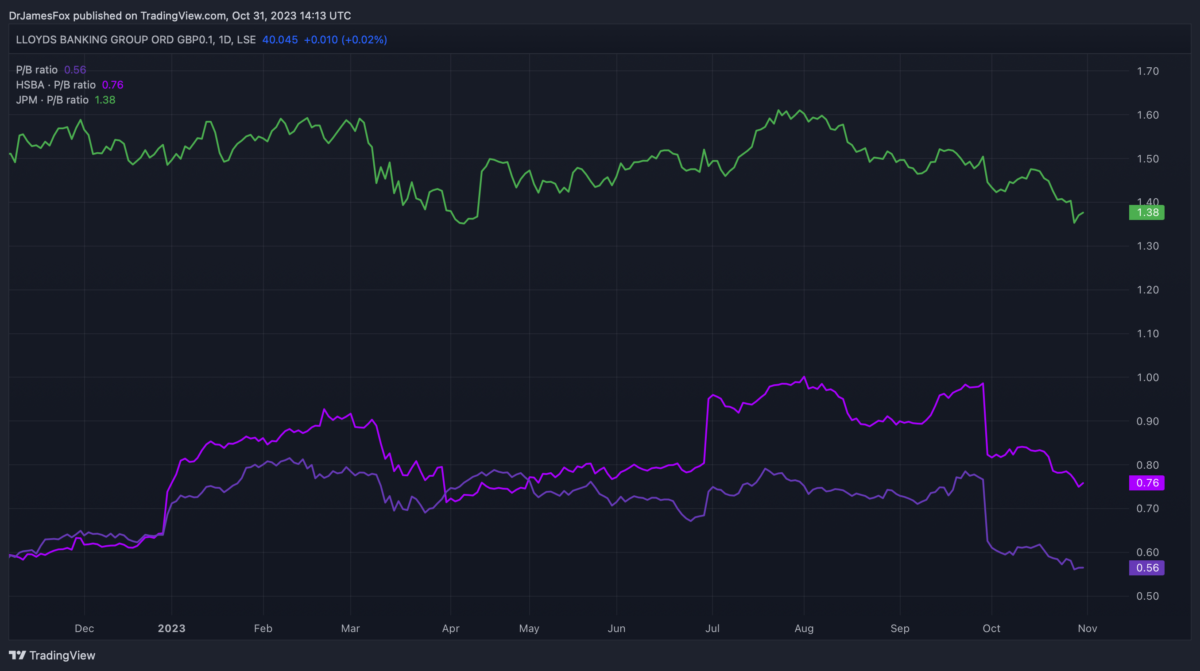

Let’s start by looking at the discount afforded to Lloyds versus peers HSBC and JP Morgan on a price-to-sales basis.

Moreover, it’s also apparent that this discount exists when we look at other metrics. Below we can see the same companies on a price-to-book comparison.

So, using some simple calculations based on these metrics, it’s not hard to see how Lloyds could be worth 80p. On a P/B and P/S basis, its broadly half the price of JP Morgan.

However, it’s not always that simple. For now, UK-focused banks are suffering from poor investor sentiment.

An improving UK economy — all of Lloyds loans are in the UK — and strengthening results in the medium term should remedy this.

Personally, I’m holding my Lloyds shares as a core part of my portfolio. If I had the capital, I’d buy more.