Rolls-Royce (LSE:RR) shares peaked at £2.33 this year, before falling back to £2. But the engineering company remains one of the strongest performers on the FTSE 100 over the past 12 months. It’s up 174.8% over the year, outpacing the index which is only up 7.2%.

So, with the stock giving back some of its gains, are we looking at a buying opportunity?

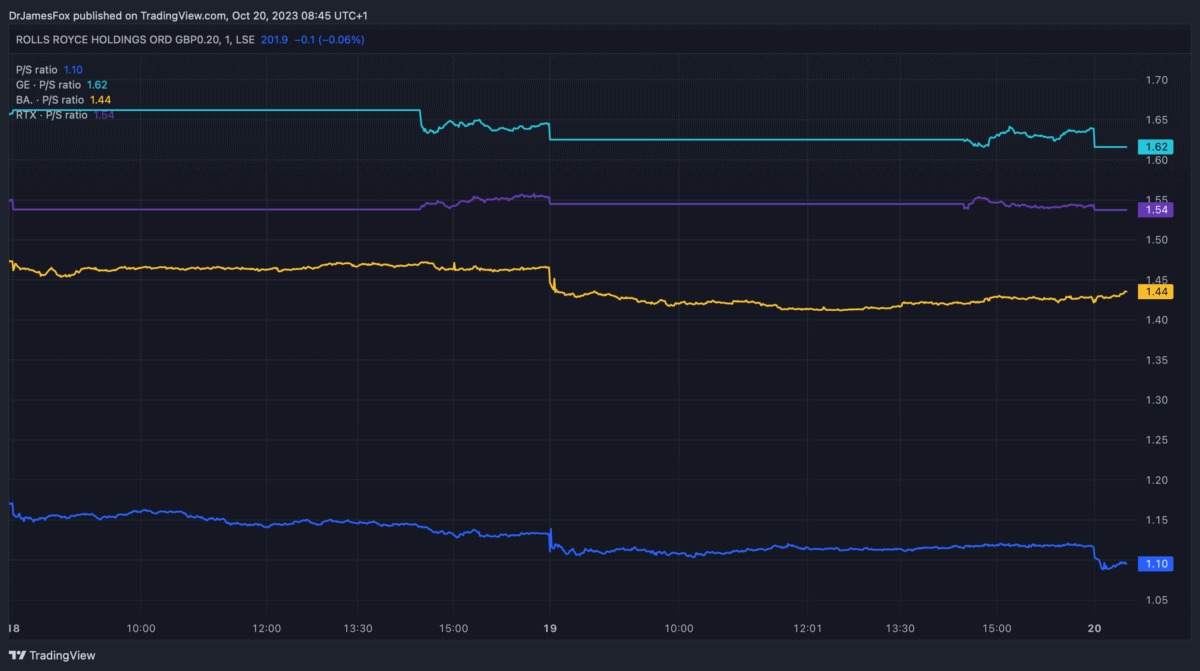

Valuation

When looking at Rolls-Royce, it makes sense to focus on metrics relating to sales than earnings given the progress of the company’s recovery from its restructuring during the pandemic.

So, we can see that the Rolls price-to-sales (P/S) ratio is 1.07 times. That’s better than General Electric at 1.62 times, and the industrials sector average at 1.3 times. Here’s how the UK engineer giant stacks up against peers including BAE Systems and RTX Corp.

As we can see Rolls still trades at a discount to its peers here, suggesting the stock could have further to rally. However, earnings are the most important metric, and analysts will be keeping a close eye on profitability.

Profit forecasts suggest earnings per share of 7.2p in 2023, 9.8p in 2024, and 12.7p in 2025. The 2023 forecast would mean a price-to-earnings (P/E) ratio of 27.8 times, which is more expensive than its peers. However, a forward P/E of 15.6 times in 2025 is cheaper than its peers.

This is broadly supported by technical data, which is more frequently used by traders and doesn’t show any warning signs.

Long-term credentials

The long-term hypothesis for buying Rolls-Royce stock revolves around the expansion of the civil aviation sector.

Civil aviation — the production, sale, and servicing, of aircraft engines — is the company’s largest business segment.

More specifically, a large part of the company’s revenue is tied to flying hours. Naturally, this part of the business suffered during the pandemic when international travel virtually stopped.

However, looking forward, the industry is expecting a huge tailwind for international travel in the years to 2042, driven by a growing global middle class, notably in developing economies.

It’s also positive that the firm’s debt appears to be much more manageable today than it was during pandemic with a current net-debt-to-EBITDA ratio of 1.5 times. Anything below three is normally considered acceptable.

In an industry whereby R&D expenses can be sizeable, improving debt is particularly important, allowing the business to invest in disruptive and innovative technologies like hydrogen power and modular nuclear reactors.

Some of these projects, like the recently cancelled carbon capture initiative, may prove unprofitable, but innovation is what drives the business.

Refocusing

One problem for the firm is that the vast majority of demand in civil aviation will be for single-aisle aircraft. Typically, Rolls-Royce’s engines are used on wide-body jets. And only 20% of the demand is forecast to be for wide-body jets.

As such, Rolls is looking to refocus its engine offerings towards this market. However, CEO Tufan Erginbilgic says the move may take a decade until the next generation of single-aisle planes are produced. Rolls, arguably mistakenly, left the narrow-body market in 2011.

While I sold my Rolls-Royce shares recently, I do recognise that the investment hypothesis remains strong. £2 might not be a bad entry point. It’s certainly something I’ll look at more closely.