I just bought Glencore (LSE: GLEN) stock. To me, it looks like the UK’s best value miner. It’s maybe even the best FTSE 100 bargain.

I was a little on the fence, I must say, as I have exposure to the mining sector already. But the evidence suggested a steal at current prices.

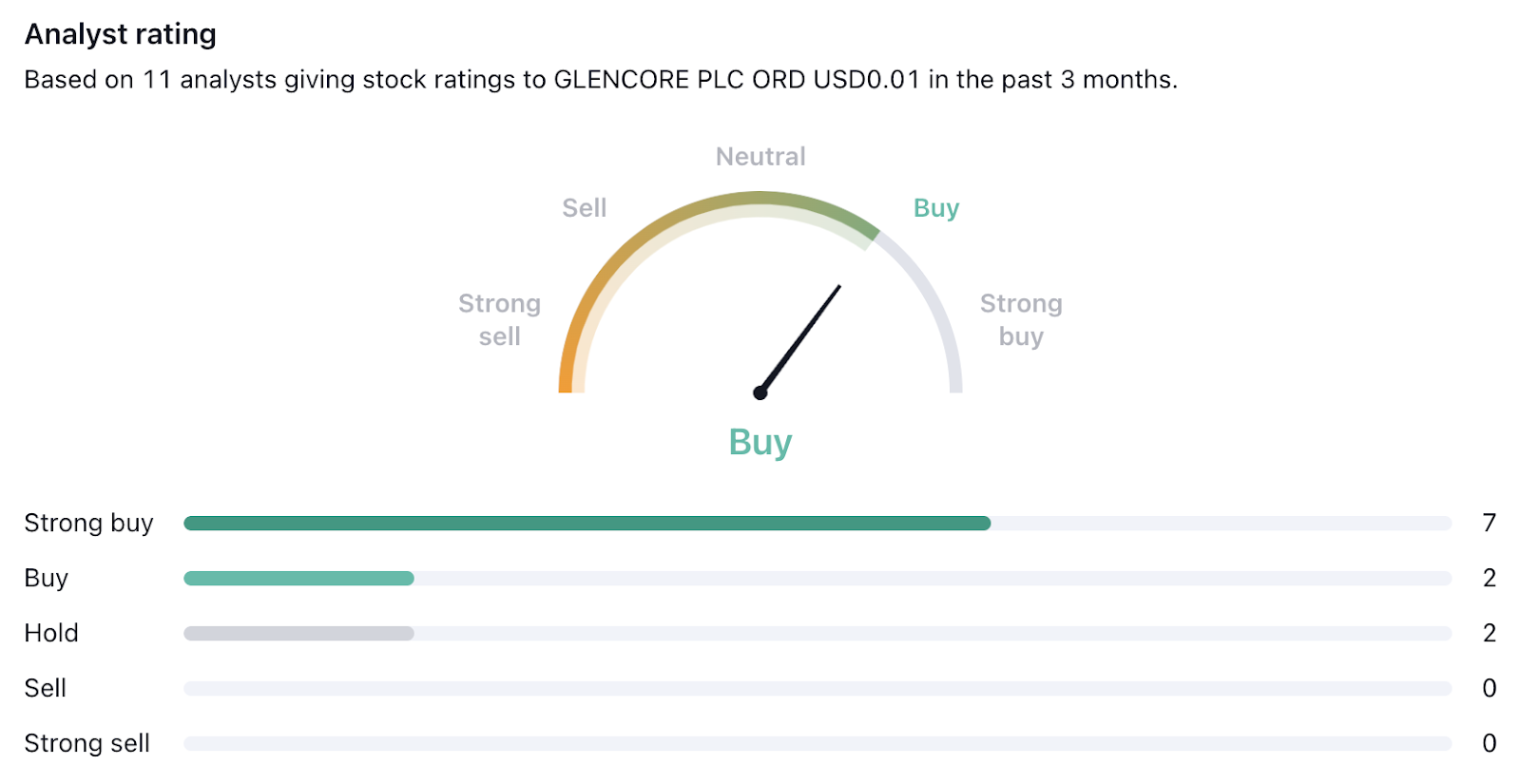

The first thing to catch my eye was the latest analyst ratings. From ratings done in the last three months, Glencore boasts seven ‘Strong buys’ and not a single ‘Sell’.

This buying consensus is perhaps sparked by a low share price. It currently stands at 440p which is 24% discount from its 52-week high. That looks like an attractive entry point.

Analysts expect the share price to swing upwards here. The average price target is 551p which would mean a 25% increase, and the maximum price target is 609p for a 38% increase.

An increase in share price sounds good already, but it won’t be my main source of income. After all, Glencore is a bona fide dividend stock. A big chunk of its profits go towards dividend payments and this is my main reason for buying.

Highest Footsie yields

The dividend yield stands at 7.86%, a figure I’m very happy with, and it was paid out from 54% of earnings last year, which seems reasonable. While the dividend is forecast to fall a little in the years ahead, I’d still expect to receive one of the highest yields on the Footsie.

Looking towards the future is more of a mixed bag. On the one hand, I’m encouraged by future demand for metals and minerals. The world needs more resources and Glencore could be at the heart of that and make my shares look like a great investment.

The following graph from Statista shows some forecasts. Copper and nickel, in particular, both comprise big chunks of Glencore’s total sales.

However, it won’t be plain sailing. Glencore just enjoyed a bumper year with record profits but that was largely down to the sale of coal amid the energy crisis. In 2022, coal made up 53% of the firm’s revenue.

Mining is a cyclical sector, so these swings aren’t unusual, but more than half of sales came from a fossil fuel the world wants to ban. That’s a risk looking forward. And earnings per share (EPS) are expected to decline in the short term.

This reliance on coal is a concern for the long term. A Net Zero 2050 target looms in the distance and activist shareholders have raised concerns about this climate-polluting resource.

It’s hard not to think of Shell’s recent pivot to producing more oil. Coal, like oil, is useful and in demand. And it’s a handy solution to an energy crisis that’s resulted from a war that doesn’t look like it’s going to end soon.

Am I buying?

Could Glencore follow Shell’s lead and focus on short term profits? Does the firm have a plan to shift towards more sustainable revenues? The answer to both questions is up in the air and the uncertainty might go some way to explaining a deflated share price.

Either way, I think the value here is too good to turn down. I’m happy I bought the shares and will cross my fingers that they’re fruitful.