A 10.5% yield! That’s how high the Vodafone (LSE: VOD) dividend has risen. It’s eye-catching, for sure, but is it a good buy?

To answer, I won’t be focusing on the short term. A single year can be misleading, and the last thing I want to do is throw my money in at the top only to see the dividend slashed and my shares tumble in value.

What I’ll do instead is zoom out a little. Doing this, with the help of charts made at TradingView, I can spots trends in that dividend. Those trends can help me see how reliable that 10% payout is. And in Vodafone’s case, I think these four charts give a very revealing answer.

What do the charts say?

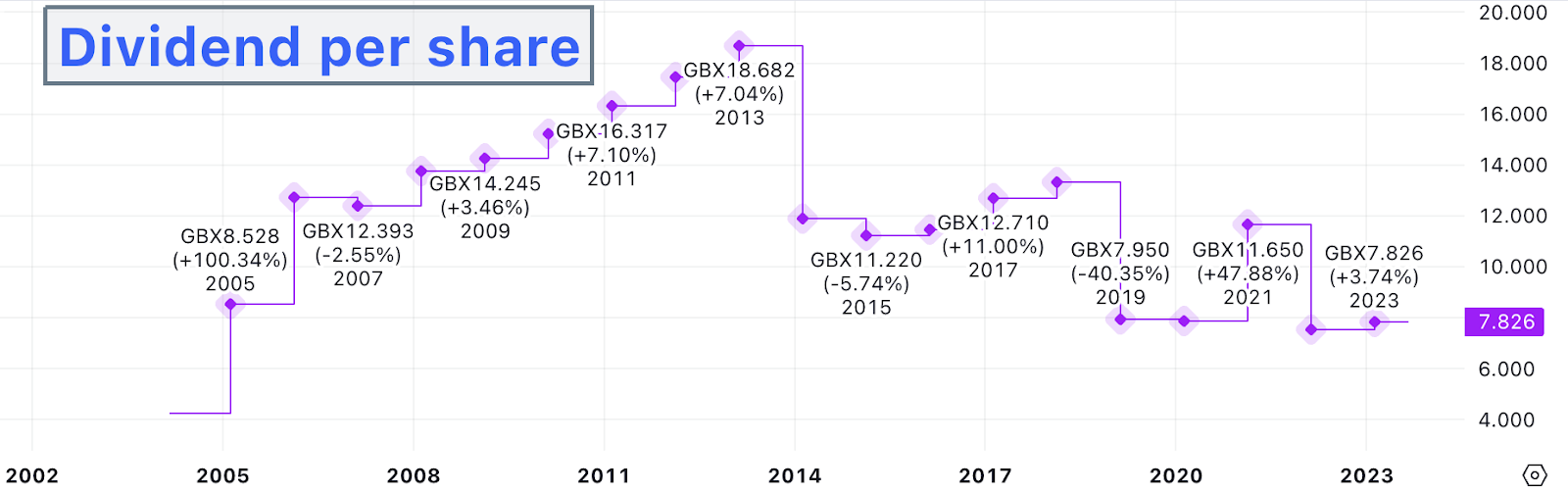

This first chart shows dividend per share. The striking detail here is that it has barely increased for years. Remember, Vodafone reports in euros, so some of the change in that graph will be due to currency conversion.

The cut in 2020 was understandable. Lots of companies did the same due to Covid. Still, the dividend does seem to be stagnating.

Not a good start, but this alone is not enough information to make a decision. Let’s explore further.

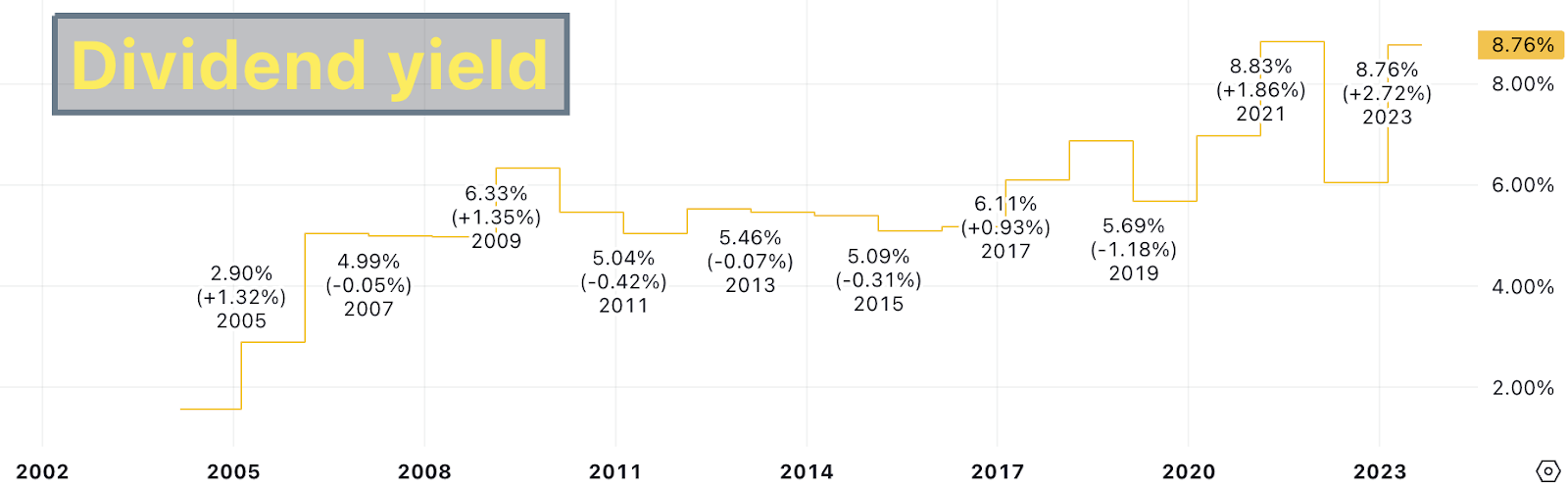

The next chart shows the dividend yield. So this is the yearly percentage return I’d get back from any investment. As we can see, it’s higher than ever. The last ‘step’ on the chart doesn’t even include the latest rise to over 10%.

Is this good? Not really. The current yield is far higher than historic levels, a red flag that investors aren’t confident in the stock. And based purely on this chart, a 5%-6% yield is more what I’d expect over the long run.

This third chart shows the dividend payout ratio. This is the percentage of earnings used to pay the dividend. And that wonky graph tells a story all on its own.

For 2021, the firm reported very low earnings which is why it’s so high. For 2020 and 2022, the ratio was above 100%, so the company didn’t make enough profits to cover the dividend. The 2023 ratio would have been over 100% too if it weren’t for the one-off €9bn disposal of one of its German operations.

In short, Vodafone hasn’t been earning enough to pay its dividends. And that brings me onto the last and perhaps most revealing chart.

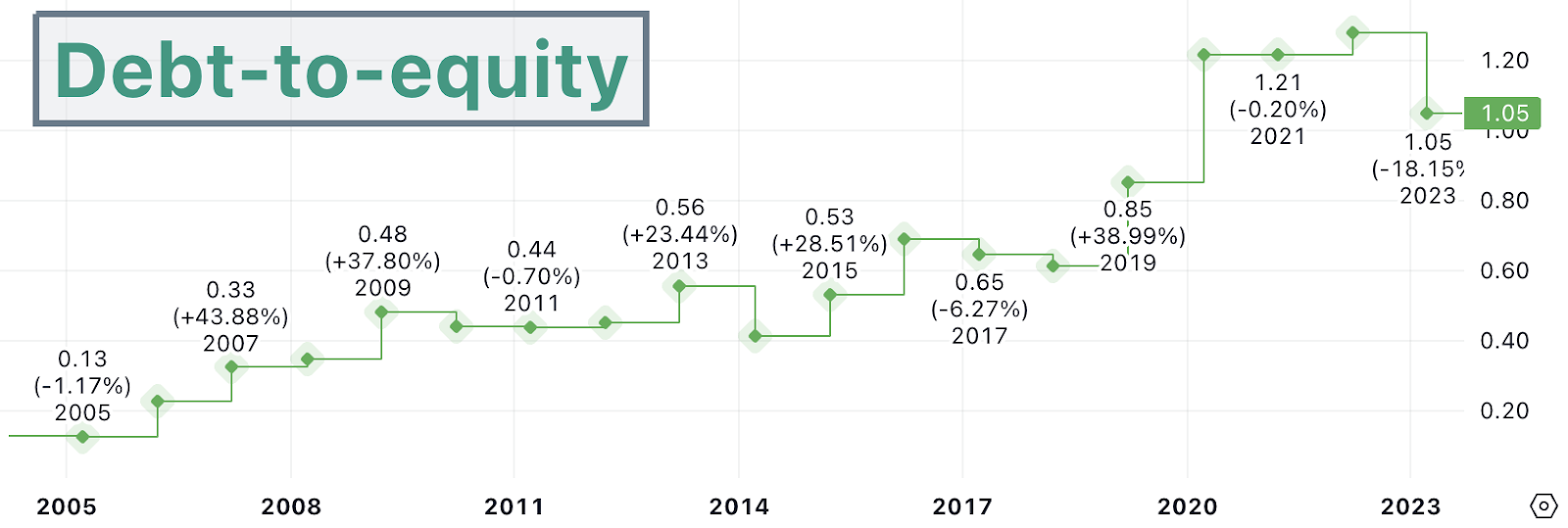

This final chart shows Vodafone’s debt-to-equity (D/E). This is how much debt the firm is in compared to the total shareholder equity. Because it’s a ratio, we can easily compare debt from year to year.

Clearly, debt levels are high right now. That’s not great for the dividend as future earnings may need to be diverted to pay down the debt or to cover financing. I will say though that competitor BT has an even higher D/E of 1.6 right now. So perhaps Vodafone’s debt isn’t too unreasonable.

A buy?

Taken together, do these charts say that Vodafone is a good buy? Well, I’d have to say no. They show the firm has its work cut out to keep up with those high dividends and that 10%+ yield looks like it’s on shaky ground to me. I’ll be avoiding.