The Aviva (LSE:AV) share price is down 13% over 12 months. The stock drove as high as £4.67 before falling to the current lows around £3.68. So what should investors make of Aviva?

Downward pressure

Aviva stock tanked in March despite reporting a better-than-expected 35% rise in annual operating profit and announcing a £300m share buyback.

The share price fell as financial stocks reacted to the collapse of Silicon Valley Bank. This raised concerns about unrealised bond losses.

However, Aviva never recovered despite there being no tangible downside related to unrealised bond losses.

Aviva, as a large insurance and financial services company, invests in bonds as part of its investment portfolio. However, like many balanced financial institutions, these bonds will be held until maturity.

Further downward pressure has likely been engendered by a series of adverse macroeconomic developments. Particularly persistent inflation and increasing interest rates are the most notably issues. This is compounded by a prevailing sense of extreme pessimism concerning the UK economy.

Earnings resilient

After Direct Line was caught out by inflation last year, investors were right to be cautious on the sector. However, earnings at Aviva have remained resilient.

In August, Aviva posted strong first-half results, with an 8% year-on-year increase in operating profit to £715m.

The Solvency II own funds generation also surged by 26% to £648m. However, the Solvency II shareholder cover ratio declined by 10 percentage points to 202%.

Meanwhile, gross written premiums rose 12% to £5.27bn, with a slight increase in the combined operating ratio to 94.8%.

In the insurance, wealth, and retirement sector, new business value grew by 7% to £319m, and operating value added increased significantly by 32% to £640m.

Additionally, the company’s IFRS profit for the period turned positive, reaching £377m compared to a loss of £198m in the first half of 2022.

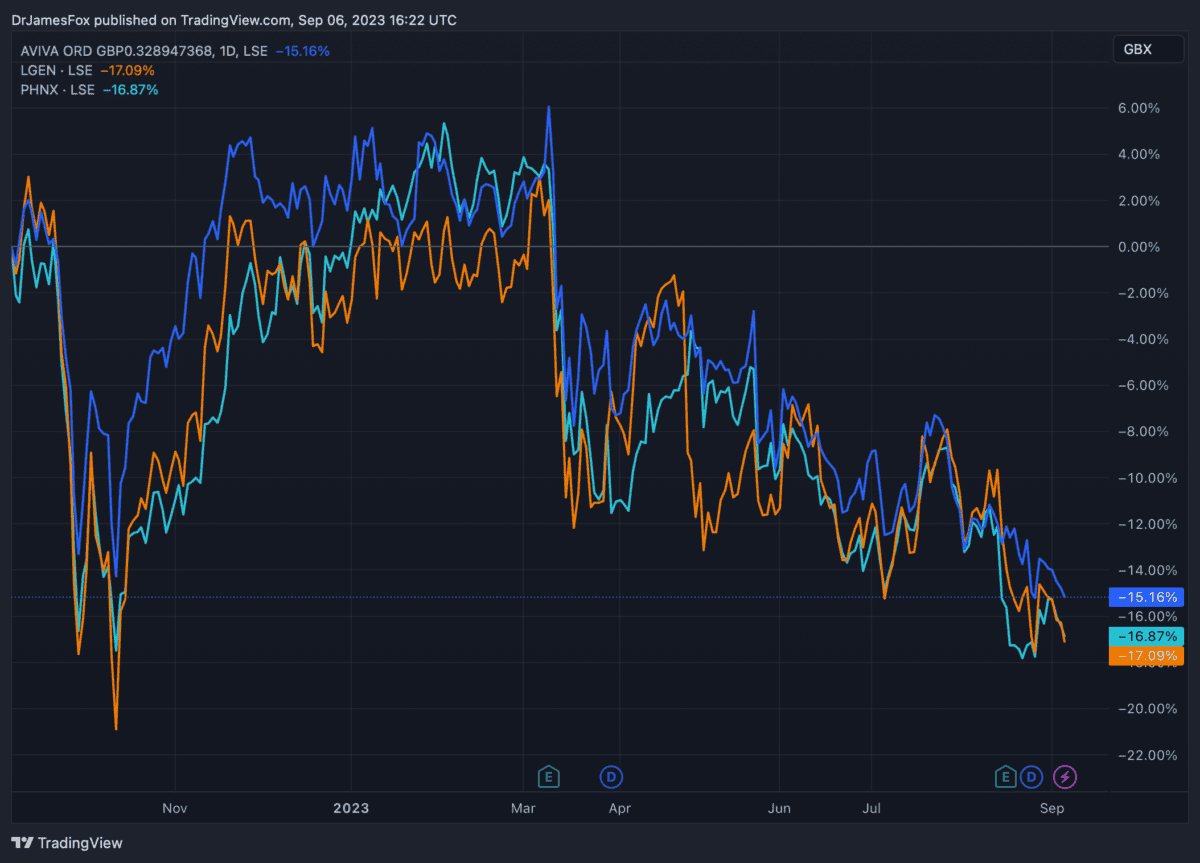

While this resilient performance hasn’t shifted the share price upwards, Aviva’s share price has outperformed its peers — although that’s not much of a consolation for investors.

The above chart shows how Aviva has fallen less than Legal & General and Phoenix Group.

Positive forecasts

According to analysts’ consensus estimates, the company is projected to achieve earnings per share (EPS) of 52.5p in 2023, which is expected to increase to 61.1p in 2024 and to 67.3p in 2025.

The Aviva share price may not have too much further to fall, thanks to its already low forward multiples. With a forward P/E of 7.5, Aviva shares are priced at nearly half the FTSE 100’s average.

Given a more optimistic medium-term outlook and the shift of capital toward equities due to declining interest rates, Aviva’s share price appears to be positioned favourably for potential growth.

Analysts’ consensus points to an average 12-month price prediction for Aviva at 533.67p, indicating a notable 53% increase from its current valuation. As such, it certainly appears that Aviva share could be worth buying.