Lloyds (LSE:LLOY) shares currently trade for 41p. That must have been almost unthinkable back in the late 90s when the stock was worth around £5 a share. Of course, a lot has changed since then.

Five-year trend

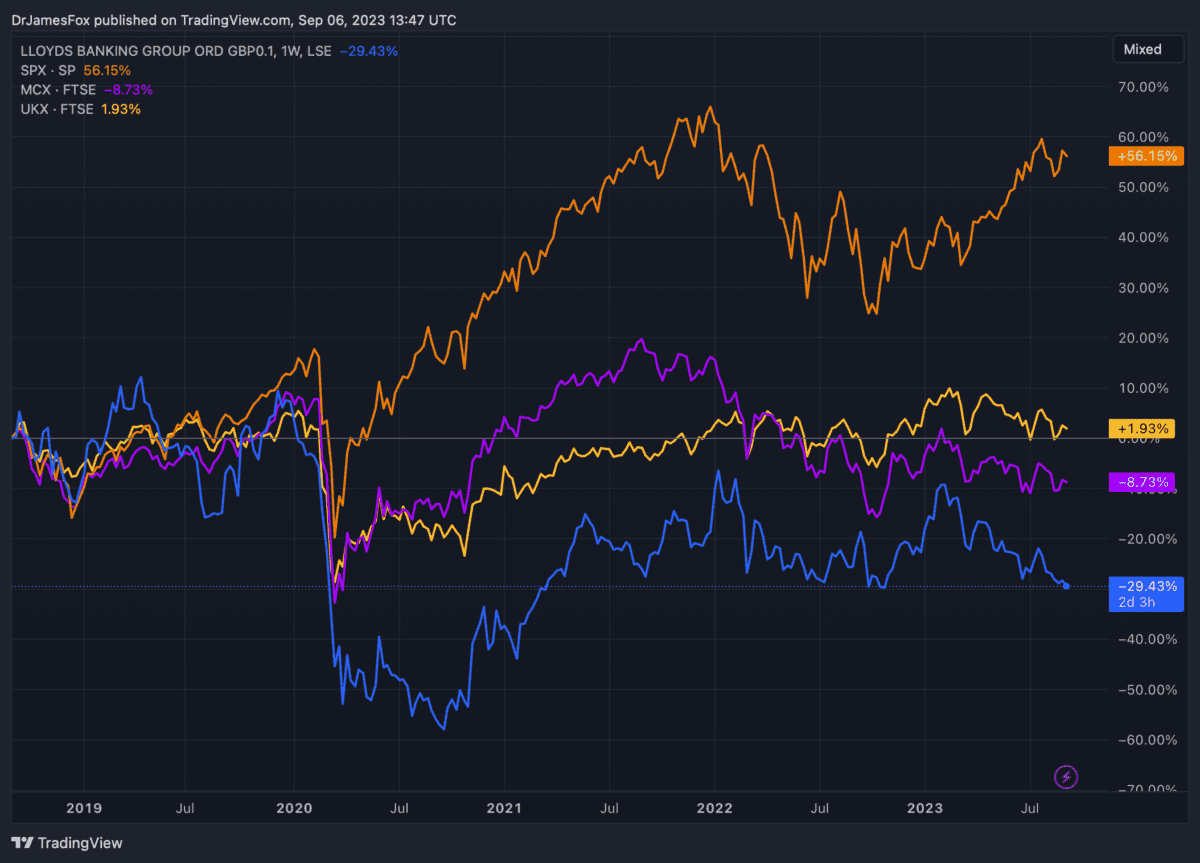

Over the past five years, the FTSE 100 has grown by 2%. That’s a very meagre return. Obviously, there have been challenges, including Brexit, the pandemic, the cost-of-living crisis, and now rising interest rates that have raised the attractiveness of debt and cash over equities.

However, Lloyds has greatly underperformed the lacklustre FTSE 100. The lender’s share price is down 29% over five years. As such, a £10,000 investment then would be worth £7,100 today. Of course, there have been dividends. I’d have recouped around £1,200 over the period.

With many investors looking for returns in the region of 8-12%, Lloyds would have been a sizeable drag on mine over the five-year period. The chart below highlights the performance of the Lloyds share price versus the FTSE 100, FTSE 250, and the S&P 500.

Headwinds and tailwinds

With the exception of the early days of the pandemic, Lloyds is trading near its five-year low. While novice investors may assume banks are performing extraordinarily well in the current high-rate environment, that’s not the case.

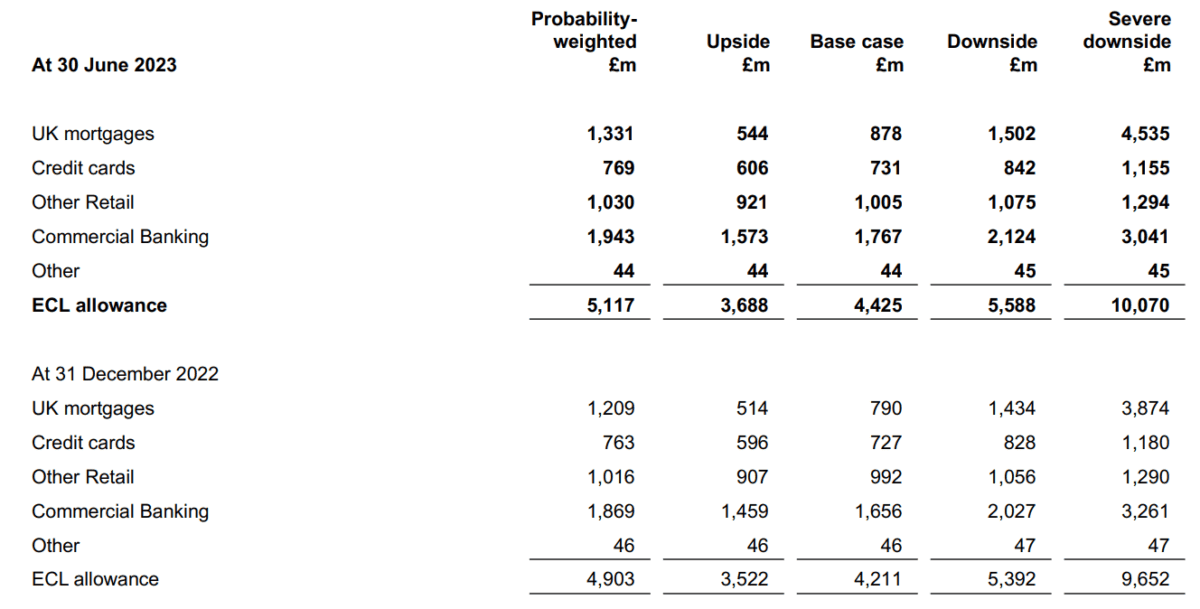

The problem is that interest rates have extended far beyond levels normally considered optimal. And this has raised concerns about the threat of mass defaults. Under Lloyds’ worst-case scenario, the bank anticipates expected credit losses of £10.1bn.

However, this is some way above the ‘base case’ outcome. Moreover, I’d hope the Bank of England would take action before we reach a mass default situation.

It’s also worth noting that Lloyds was the second-best-performing bank in the recent stress test. In the stress scenario, Lloyds’ CET1 would decline to 11.6%, placing it ahead of all banks except Nationwide –Lloyds’s CET1 ratio fell from 14.7% (as noted in the stress test) to 14.2% in the H1 results.

To date however, the tailwind associated with higher rates — higher net interest income — has surpassed impairment charges.

In H1, net interest income rose 14% to £7bn versus £6.1bn last year. Meanwhile, Lloyds impairments rose 76% to £662m in H1. Consequently, underlying profit before impairments rose 16% to £4.7bn.

Undervalued

Despite the concern about mass defaults, data suggests that the bank is oversold and that it remains meaningfully undervalued. The lender trades at 5.2 times TTM earnings and 5.6 times forward earnings. This makes it one of the cheapest company’s on the FTSE 100.

Not having an investment arm, Lloyds is more exposed to the interest rate climate than its peers. However, this doesn’t account for the size of the discount versus its international peers. The global banking sector trades on TTM multiple of 9.4 times and forward multiple of 9.7 times.

As with any investment, there is risk. However, the risks appear to be more than priced in.