Let’s say I had zero savings. Nothing in my bank account. No investments or anything like that. Even in this case, I think I could target a £27,756 second income.

That number is the median wage, so it’s a lofty goal to aim for, but it’s also a big ask from a standing start.

What I’ll need to do is use the wealth-building power of stocks. If I invest in a stock, I can watch my wealth grow as the company grows. This can be a fantastic method of multiplying my money, but it also is not risk-free.

I can lose money with stocks, and companies go bust all the time. Carillion, Cineworld, and Thomas Cook are all ones that have gone bankrupt in the last few years. Anyone holding the shares lost everything they put in.

So, the core part of my second income strategy will be to limit this risk.

Before I get to that, how much money would I need? Well, a rule of thumb is I can withdraw 4%. That figure is considered a ‘safe withdrawal rate’. It’s lower than what I’d hope to get back from investing in stocks, so I can pull out a second income and my nest egg would stay intact or perhaps grow further.

26 years

Working backwards, I’d need £693,900 to achieve a £27,756 yearly second income. That sounds like a lot. Even if I save £500 a month, it would take 112 years to get there. I’m not building this income for my great-grandkids, so I’ll need a faster method. This is where investing comes in.

Now, let’s say I still save £500 a month, but I get an average 10% return from stocks. That return will slash the time it takes. Crunching the numbers, it looks like it would take a smidge over 26 years.

Right, so 26 years for a £27,756 second income? That sounds pretty good, especially compared to over 100!

Of course, it’s not easy to save £500 a month. The number is arbitrary though. I could aim for a smaller target and still reap similar rewards.

So far, so simple. But there is the question of risk. How would I do this without losing money or making a bad investment?

Well, I’d start with total market index funds. This is like investing in a whole stock market, so it spreads out my risk across tonnes of companies. A bankruptcy here or there won’t make much difference.

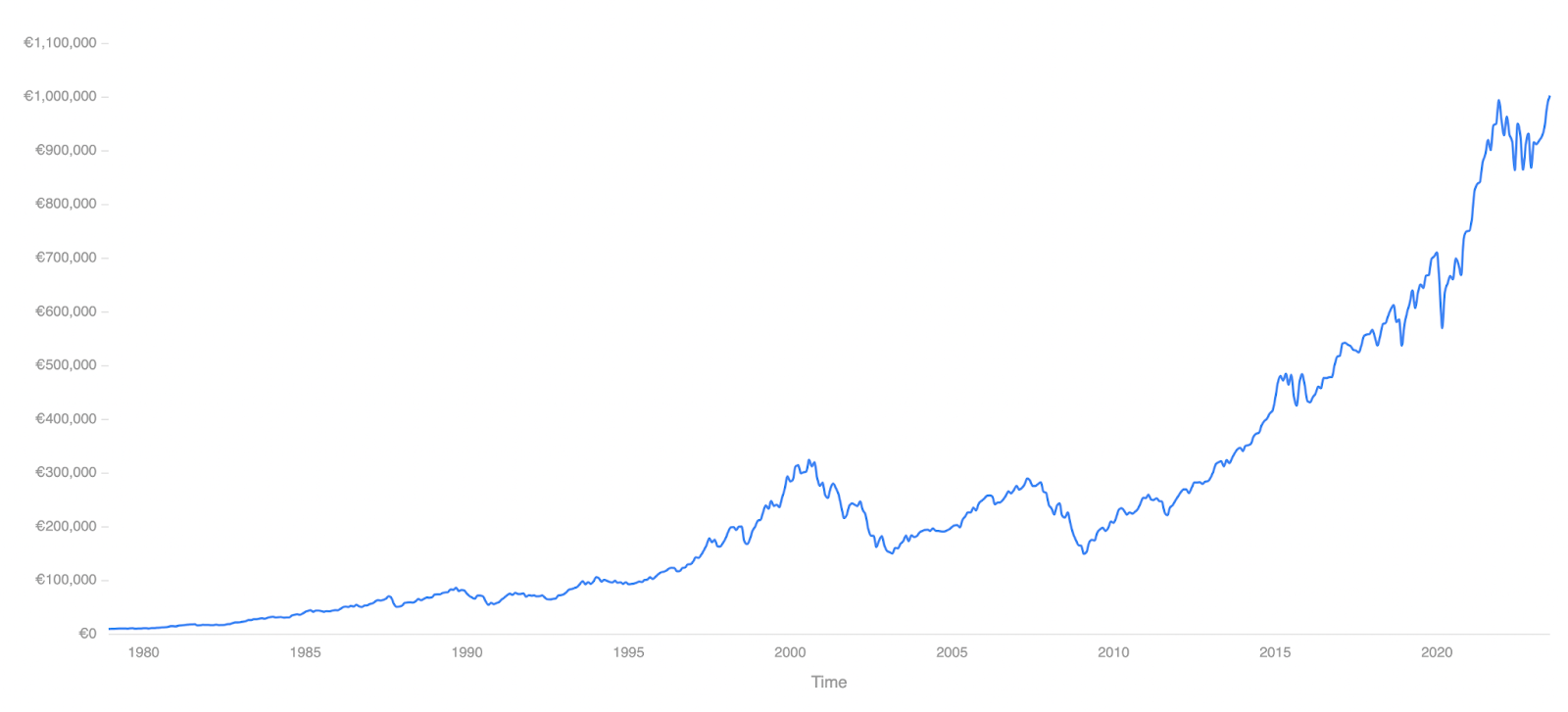

A stock market can crash, of course. But it’s pretty unlikely an entire economy will crash for long periods. Here’s a look at the S&P 500 over the last 45 years. There are some huge crashes in there, recessions and economic crises too. Long term though, each one is little more than a blip.

My move

Once I feel more comfortable, I can start to put some money into individual companies. This offers me the chance of higher rewards so I could get to my goal faster.

the portfolio I have now is a blend of index funds and individual stocks. This offers a lot of safety while still having a good chance to beat the market. Will I one day pull a £27,756 income from it? I hope so.